If you own or operate a private company in Australia, it’s important to be aware of Division 7A (Div 7A) loans and how they affect the way you take money out of your business. Division 7A is a provision in the Income Tax Assessment Act that was introduced by the Australian Taxation Office (ATO) to prevent company profits from being distributed to shareholders (or their associates) in a way that avoids tax.

Put simply, when a private company lends money to a shareholder, makes a payment on their behalf or forgives a debt, the ATO may treat that transaction as if it were an unfranked dividend – unless it is structured correctly as a compliant loan. To remain compliant, the loan must be set out in a formal agreement, meet the ATO’s minimum interest rate requirements and follow a strict repayment schedule.

Why does this matter? Without proper planning, a simple transaction – like borrowing from your company to fund a personal expense – could lead to unexpected tax bills. Understanding Div 7A ensures business owners and shareholders can manage their cash flow efficiently while staying on the right side of the tax rules.

We get lots of questions about this so let’s break it down in detail.

What is Div 7a?

Division 7A, often shorted to Div 7a, is a set of tax rules developed by the Australian Taxation Office (ATO). It aims to prevent private companies from distributing profits to shareholders or associates of shareholders tax-free. This can include loans, payments or forgiven debts. Understanding Division 7A helps ensure compliance and avoid penalties.

Essentially, it was established to ensure that shareholders don’t try to disguise dividends and pay the appropriate amount of tax.

What is a Div 7a Loan?

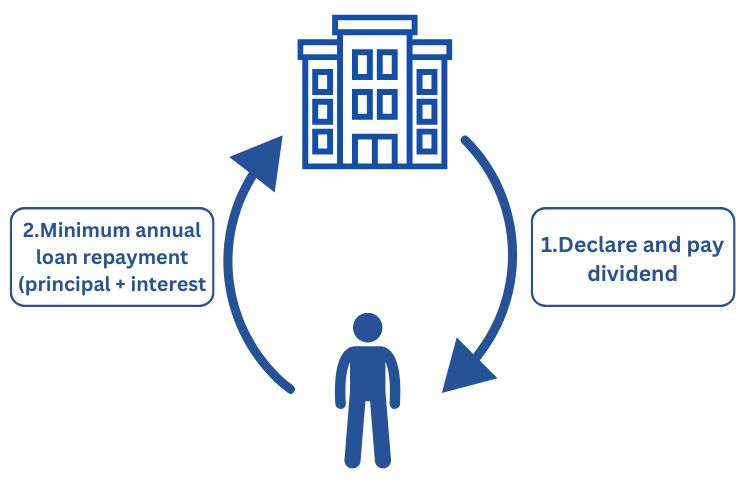

A Div 7A loan is a formal loan agreement between a private company’s trustees and a shareholder of the company. It should be set up when the company lends money, makes a payment or forgives a debt owed by a shareholder (or their associate) in a way that is treated as if it were an unfranked dividend.

Under Australian tax law, Division 7A is designed to stop company profits from being accessed tax-free by individuals. If such a loan is not properly structured and repaid according to the Australian Taxation Office’s (ATO) rules – usually requiring a formal loan agreement, set interest rates and regular minimum repayments – the amount can be taxed as income to the recipient. In simple terms, a Div 7A loan is the ATO’s way of ensuring money taken out of a company by its owners is either repaid on commercial terms or taxed fairly.

What Triggers a Division 7A Problem?

A Division 7A problem can be triggered in several ways, each having its own set of conditions and implications:

Loans to Shareholders or Their Associates

If a private company extends a loan to a shareholder or an associate, it may be deemed a Division 7A dividend under certain conditions. This applies when the loan is not repaid by the end of the company’s income year or when it fails to comply with specific repayment terms set by the ATO. It’s essential for business owners to be aware of these conditions to avoid their loans being classified as dividends.

Moreover, the ATO specifies that loan agreements must be in writing and the terms must be strictly followed to avoid reclassification. Failure to comply can result in the loan amount being treated as an unfranked dividend, which can have significant tax implications for both the company and the borrower. Therefore, establishing clear, compliant loan agreements from the outset is crucial.

Payments Made by the Company

When a company makes a payment to a shareholder or their associate, and it is neither a dividend nor related to services rendered, it may trigger Division 7A. This includes payments for personal expenses, which are often overlooked by business owners. Such payments, if not properly accounted for, can lead to unexpected tax liabilities. In addition, this may result in a Fringe Benefits Tax bill if the shareholder is also a director of the company or an employee of the company.

To prevent this, it’s important for companies to maintain detailed records of all transactions and ensure that any payments made are either properly documented as dividends or relate directly to business operations. Proper accounting practices and regular audits can help in identifying such payments and addressing them before they become an issue.

Debt Forgiveness

Debt forgiveness is another trigger for Division 7A. If a company forgives a debt owed by a shareholder or an associate, the forgiven amount is considered a benefit akin to a dividend. As such, it is subject to taxation under Division 7A. Business owners must be cautious when forgiving debts and should consider the tax implications before proceeding.

Forgiving a debt may seem like a straightforward decision to alleviate financial or tax strain for a shareholder, but without proper documentation and consideration of Division 7A, it can lead to significant tax liabilities. Consulting with a tax professional before forgiving any debt can help business owners make informed decisions and avoid adverse tax consequences.

Managing A Division 7A Loan Agreement

Effectively managing Division 7A loans is vital to ensure compliance and avoid unexpected tax liabilities. Here are some key strategies to consider:

Establishing a Compliant Loan Agreement

To prevent the loan from being treated as a dividend, establishing a formal div 7A loan agreement is essential. This agreement should detail the loan amount, interest rate, and the loan term. The interest rate must meet or exceed the ATO’s benchmark interest rate, and the loan term should not exceed seven years for unsecured loans and 25 years for secured loans.

Having a compliant loan agreement serves as a safeguard against reclassification and potential tax penalties. Regularly reviewing and updating these agreements to align with any changes in ATO regulations is also crucial. This proactive approach ensures that the terms remain favorable and compliant throughout the loan’s duration.

Calculating Minimum Repayments

Each year, a minimum repayment must be made on a Division 7A loan to prevent it from being treated as a dividend. This repayment includes both principal and interest. Utilising a Division 7A loan calculator can help determine the exact repayment amount required to stay compliant with ATO regulations.

Timely repayment not only ensures compliance but also aids in maintaining the financial health of the business. It demonstrates a commitment to meeting financial obligations and can positively impact the company’s creditworthiness and relationships with stakeholders.

Making Repayments Before the Lodgement Date

Ensuring that the minimum repayment is made before the company’s tax return lodgement date is crucial for maintaining compliance and avoiding the loan being classified as a dividend. This proactive approach helps in mitigating potential tax liabilities and demonstrates responsible financial management.

Regular monitoring of repayment schedules and setting reminders can aid in meeting these deadlines consistently. Moreover, integrating repayment schedules into the company’s overall financial planning can streamline processes and prevent last-minute scrambles to meet compliance requirements.

Regularly Reviewing Loan Agreements

Regularly reviewing the terms of the loan agreement is essential to ensure ongoing compliance with the latest ATO regulations. This includes checking the interest rate and repayment terms to ensure they remain in line with current standards.

Frequent reviews allow business owners to address any discrepancies or changes in regulations promptly. This not only prevents potential compliance issues but also facilitates informed decision-making regarding future financial strategies and adjustments.

Does Division 7A Apply To Trusts?

A common question among business owners is whether Division 7A applies to trusts. While Division 7A primarily targets private companies, it can also apply to trusts if the trust is a shareholder or associate of a shareholder in a private company. In such cases, trust distributions made to a company (e.g. distributions made to a “bucket company” to cap the tax applied to the company tax rate) can be subject to Division 7A if they are unpaid and the trust is considered an associate of the company.

Understanding the implications of Division 7A on trusts is crucial for businesses that operate through trust structures. Proper accounting and documentation practices are necessary to ensure that any distributions made through trusts are compliant with Division 7A. Consulting with a tax professional can provide valuable insights and help in navigating the complexities involved.

Practical Division 7A Examples

To better understand Division 7A, let’s explore a couple of practical examples:

Example 1: Loan to Shareholder

Suppose a private company loans $50,000 to one of its shareholders. If the shareholder does not repay the loan by the end of the financial year and there is no formal loan agreement, the ATO could treat this loan as a dividend, subject to tax. This highlights the importance of having a compliant loan agreement in place to avoid such tax implications.

This example underscores the need for clear communication and documentation in financial transactions within a company. By establishing formal loan agreements and ensuring timely repayments, businesses can prevent reclassification of loans and avoid incurring unnecessary tax liabilities.

Example 2: Payment for Personal Expenses

A company pays $10,000 for a shareholder’s personal vacation expenses. If this payment is not declared as a dividend or included in the shareholder’s assessable income, it may be treated as a Division 7A dividend. Proper accounting and documentation are essential to prevent such reclassification and the resulting tax implications.

This scenario highlights the importance of maintaining transparency and accuracy in financial records. By ensuring that all transactions are properly documented and accounted for, businesses can avoid potential issues with the ATO and maintain their financial integrity.

Division 7A FAQs

Division 7A is a tax provision that applies when a private company provides a loan, payment or debt forgiveness to a shareholder or their associate. If the transaction is not structured correctly, the Australian Taxation Office may treat it as an unfranked dividend and tax it as income.

The Division 7A benchmark interest rate is set each year by the Australian Taxation Office. For the 2025 income year the rate was 8.77%. For the 2026 income year the rate is 8.37%. This rate must be applied to complying Div 7A loans to ensure they are not treated as taxable dividends.

Yes, interest paid on a Division 7A loan can generally be deductible if the borrowed funds are used for income producing purposes such as investing or running a business. If the loan is used for private purposes the interest is not deductible.

To avoid paying Division 7A interest you need to ensure that any loan from a private company is repaid in full before the company’s tax return lodgement date. Alternatively you can put in place a compliant loan agreement that meets the ATO’s requirements for minimum yearly repayments and benchmark interest rates.

Yes, Division 7A can apply to trusts in certain situations. If a trust makes a distribution to a private company and the funds are instead used by the trust or its beneficiaries without being paid to the company, this can trigger Division 7A rules.

If a private company forgives a Division 7A loan, the amount forgiven is generally treated as an unfranked dividend. This means it will be included in the borrower’s assessable income for tax purposes.

Yes – you can access the ATO Div 7A calculator to help you understand your obligations

Conclusion

Understanding Division 7A is essential for small business owners to ensure compliance with Australian tax laws and avoid unexpected tax liabilities. By establishing compliant loan agreements, making timely repayments and regularly reviewing terms, you can effectively manage Division 7A loans.

The tax team at MGI South Qld can help you to navigate the complexities of Division 7A and make informed decisions for your business. Understanding these regulations not only protects your business from potential tax issues but also contributes to a strong foundation for long-term success.

Contact our team today to ensure your company avoids unnecessary tax penalties.