Subscribe for Our Latest Resources

"*" indicates required fields

Are you losing staff due to higher alternative salary rates on offer in the market? Then offering performance based rewards will assist you to retain staff and improve your bottom line!

Research indicates Generation Y has high earnings expectations and wants rewards based on performance. To implement an effective performance based rewards program, your staff needs to have input and agree to what is expected of them (“deliverables”).

Establish the deliverables for both individuals and team positions. These can include a range of quantitative (objective) and qualitative (subjective) assessment criteria. Once the deliverables are agreed, you will apply a weighting to each criteria. This will depend on the strategic and operational objectives of your business (grow sales, new customers, better productivity etc). A staff member’s result determines the amount of their performance bonus. The more they deliver the higher their rewards. It’s a win for both owners and their staff.

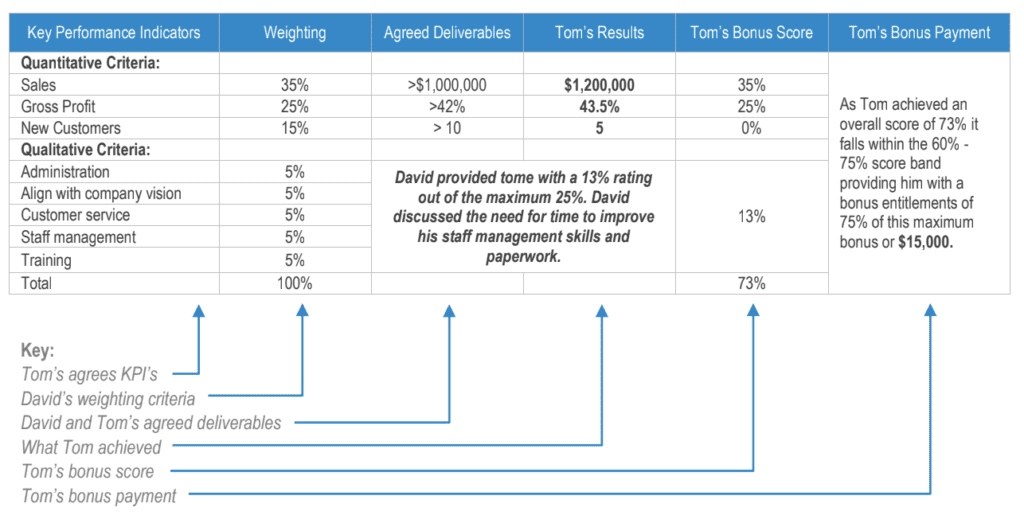

David needs to grow sales and improve profitability. David’s concern is his staff costs are increasing and profits are declining. He has now implemented the Staff Value Program and agreed to pay Tom, a key staff member, a maximum bonus of $20,000. The payment of the bonus is conditional upon Tom meeting specific performance targets. Below is his bonus score card.

The qualitative assessment process allows business owners to assess the achievements of their staff and the criteria are measurable by observation. It provides a proactive approach for addressing subjective performance matters that are otherwise usually left unresolved.

Once the Staff Value Program is implemented by your business, you then need to ensure you have the systems and procedures in place to measure your staff’s performance on a timely basis. As performance bonuses are paid as a result of exceeding budgeted profits, business owners are beginning to realise they can compete with apparently higher alternative salary rates on offer in the market and retain their staff by paying a sufficient bonus based on performance.

The business advisory team at MGI have specialists who have helped businesses like yours develop a performance based reward program. A business coach from MGI can help you to implement a similar scheme and help improve your staff retention. We always have a clear focus on managing costs and improving profitability. We offer expert business growth support and can also assist with business benchmarking and analysis to ensure your business remains competitive.

You’ve grown your business gradually and now your minds turn to collecting your reward from your investment capital, know-how, and years of effort. Achieving the most for your business requires the same diligence it took grow it. This is where having a business succession plan becomes vital.

Developing a effective plan for business succession is the key protecting, growing and realising the maximum value for your business. It is a strategic process that allows you to smoothly transition the ownership and/or management for your business.

Research shows that business value can be impacted by a number of issues including:

Times change, markets change, and so does the business environment. Not long ago, business entry costs and competitive forces were lower and business growth could be funded by borrowing against increasing house prices.

Business success demands focus by you on the operation, but ultimately, issues of success and retirement will creep up. By then, getting the price you need could be elusive.

The next generation of business owners, Generation Y, face a completely different business environment. Start-up and acquisition costs are higher, regulatory barriers are higher, and competition has increased. Business funding opportunities are also more limited in comparison.

You’re a business owner and you understand the driving forces behind competition, supply and demand.

So when do you need to start developing a plan for business succession?

Thus, it is important for you to start planning your succession now. Talk to the business advisory team at MGI about our succession planning services and let us help you start the process. We can help you benchmark your business against others in the market, strategic planning planning, wealth management and business valuations.

You might also be interested in our previous blog about business exit strategy.

One of the reasons businesses run out of cash – and generally go broke – is that they grow too fast. What a paradox – the business is growing too quickly and is therefore too successful for its own good! Not surprisingly, in situations like these you also find that the largest “creditor” of the business has been the Australian Taxation Office, due to either unpaid tax liabilities. In other words, the business has used the ATO as a banker. The obvious question is – why? The broader answer is very simple – lack of access to alternative funders. Debtor financing or debtor funding is one of the options that is generally not explored – but could be a reasonable solution.

A typical family-owned business usually only has two main sources of funding – the owners or the bank – and the latter option is generally only available if the owners have “bricks and mortar” security (i.e. their home).

Where the business owner has little or no equity in their home and/or the funding needs of the business exceeds the amount they can borrow against their home, the options tend to be very limited. Banks may still lend something against the assets of the business (e.g. stock and debtors), but the size of this facility is often a fraction of the assets pledged as security and the facility may not increase as the cash flow needs of the business increase.

Children taking over a business from their parents may also lack the amount of capital (or property security) needed to grow the business.

Family-owned businesses are also reluctant to call in a “white knight” (a friend with cash) or venture capital provider. In any case, the latter are generally not attracted to smaller “mum and dad” family businesses. This therefore only leaves two sources of funding – business creditors and the ATO. Business creditors tend to get looked after as the business owner wants to ensure supply of raw materials to their business, which just leaves the ATO. However, you ought to be aware of recent changes made by the ATO in relation to tax debt interest charges.

One often overlooked source of funding may be to “borrow” against the debtors of the business through a debtor finance arrangement (previously called factoring).

Traditionally thought of as a lender of last resort, debtor finance companies should not be overlooked as a source of funding for growing businesses, provided the business is profitable. The latter point is crucial, because it is no use accessing cash flow (from anywhere) if the business is not making money. The cash will soon run out and the business will go broke. This was also another reason provided in one of our previous articles about why businesses don’t have cash – they don’t have a cash flow problem, they have a profitability problem. A lack of cash is the symptom, but a lack of profitability is the cause.

Assuming the business is profitable and growing, debtor finance provides an opportunity to borrow against the debtor book, particularly where it is a high quality debtor book. Generally, debtor financing companies will advance a percentage of the debtor book (e.g. 75% or 80%) for those debtors who have been outstanding for less than 90 days.

Debtor financing offers a wealth of advantages for growing businesses:

Free up cash tied up in outstanding invoices—typically between 70–90% of the invoice value is released upon submission—enabling you to cover wages, supplier costs, or invest in opportunities without waiting for payment terms to end.

As your sales increase, so does your finance limit – making debtor funding more flexible than traditional loans constrained by physical collateral.

You’re not required to pledge property. Instead, lenders use your invoices as security, making debtor finance ideal for entrepreneurs without bricks-and-mortar assets.

With invoice factoring, your finance partner often handles debtor collections—leaving you to focus on core business activities.

Access to funds aligns with invoice generation, and repayments occur only when customers pay. It’s a financing model that adapts seamlessly to your business’s rhythm.

Often quicker to arrange than traditional bank loans, debtor finance is well-suited to companies without extensive asset backing or high turnover.

Understanding the main forms of debtor funding helps you choose what best fits your operation:

You sell your invoices to a finance provider.

The provider collects payment directly from your customers.

Common advance rates range from 70% to 95%, typically with higher fees due to the additional credit control service

Ideal for small or mid-sized businesses that prefer not to chase payments themselves

You borrow against your invoices while retaining control over collections.

Customers remain unaware of the arrangement.

Advance rates typically sit around 80–85%, with lower fees than factoring

Suited for larger businesses with in-house credit teams

Full‑ledger: finance provider supports the entire receivables ledger.

Partial‑ledger: you select which invoices to finance (even on single‑invoice basis)

Full‑ledger offers simplicity; partial provides more flexibility and control.

There are a probably number of reasons for this. One reason might be the perceived stigma. Often, debtor financing companies will require that the arrangement be disclosed to the customers of the business and collection of the outstanding debts is handled by the debtor finance company. Whilst this needs to be carefully managed, there could be a “good news story” in here for the business and that story should be “sold”. The business is growing! Every business owner understands that a growing business needs to fund cash. So should your customers.

Secondly, the business is “outsourcing” its debtor management, thereby enabling the owners to focus on doing what they do best – build the business. You may also find that your debtors are better managed (and more likely to pay on time) when there is greater focus applied.

Another reason may be because debtor finance is generally a more expensive form of funding than traditional bank finance secured by a property. This is not surprising – it’s more risky. If the business owner had property to put up as security then they wouldn’t need debtor finance. So it is important to understand what the cost of funds will be. Even if the effective cost of funds is (say) 15%, provided the business is making a return on capital employed (ROCE) of greater than this then they are in front. In other words, if the ROCE for the business is, say, 25% then the business owner is still in front by 10% once the financing cost has been paid. Would you rather make 10% of something or 100% of nothing?

Clearly, in a perfect world having access to an unlimited supply of cash is utopia. However, we don’t live in a perfect world and business owners frequently have to deal with imperfection. The challenge for business owners using any sort of funding, but particularly debtor funding is to know the key financial parameters of their business.

At MGI South Queensland our specialist business growth advisors in Brisbane and on the Gold Coast can help you avoid many of the pitfalls of growing your business and ensure you maintain a healthy business cash flow.

We’re also able to offer outsourced CFO services which can be completely tailored to the needs of your organisation. From cash flow planning and management to helping you reduce the risks your business is exposed to, talk to one of our CFO consulting partners today.

This blog was first published in October 2016 and updated in April 2025.

Disclaimer: This information is general in nature and does not take into account your individual objectives, financial situation, or needs. You should consider seeking professional advice before making any financial decisions.

It’s usually easier to look back after a business has failed and identify why, than it is to save a struggling business from failing in the first place. In my view there are a number of reasons for this, not the least of which is the fact that everyone is always wiser with the benefit of hindsight.

However, it begs the question of what a business owner can do if their business is struggling? After all, they have a lot of their heart and soul invested into the business (as well as their capital). It’s their “baby” and they are convinced they’re onto a winner, even if it isn’t working out.

The answer is – it depends. It depends on many variables including what type of business they’re in, what industry it’s in, where it’s located and what size the business is and what stage it is at in its lifecycle. In my experience, scale can often play a huge part. There are many struggling business owners out there – some might call them micro businesses.

But there is hope. Here are my top four tips to get your business back on track.

When I walk past retail outlets (clothing shops for example), I often wonder if the owner knows how many (or what dollar value) of clothes they must sell each and every day in order to simply breakeven.

One thing many businesses fail to do before even setting up business is a simple breakeven analysis. A business broadly has two types of costs – fixed and variable. As the name suggests, fixed costs are largely fixed in nature. This means you’ll have to pay these whether you sell one item or one million. Whilst all costs are variable over time, rent might reasonably be regarded as a fixed cost. You will have this cost even if no customers walk in the door.

Variable costs are simply those that vary with your sales volume. If you are a wholesaler or retailer, the cost of your product might be a variable cost.

So, tip number one would be to understand your breakeven sales point (on a yearly basis) and then break this down to a daily or weekly basis i.e. how many items do you have to sell each day or each week. Then develop and implement strategies to help you sell more than this quantity.

A struggling business might be able to grow its way out of trouble, but do you have the necessary cash to fund that growth? Do you know how much cash you’ll need to fund your desired growth?

In order to answer that question you need to know one critical measure – your working capital burn rate. If you don’t know this you’re flying blind. I often see businesses targeting a certain percentage increase in sales. When I ask them how much working capital they’ll need to fund that growth they often don’t know. Sales generally don’t fund themselves.

For some businesses their working capital burn rate can be quite high. These businesses will struggle to fund rapid growth. For others it can be quite low, in which case they will have an easier road.

You need to know yours.

Every business has what I call financial drivers. If you don’t know yours you may as well be driving a car without an instrument panel on your dashboard. You don’t know how much fuel you have, whether your engine is overheating or whether your oil is getting low. It’s the same with your business.

Various businesses respond differently to a given intervention. In other words, some businesses are volume driven – they perform better the more goods they sell. Others are margin driven – they don’t necessarily need to grow at the same rate, but they make more profit on the items they sell. Once again, how your business responds will depend on a number of factors including the current size of your business and your breakeven level.

Some businesses require large amounts of working capital e.g. stock and debtors, and can therefore respond well to small improvements in working capital management. Others may have what is called a lazy balance sheet, with a number of underperforming assets.

The key is to understand your key financial drivers – changes in these areas will give you the biggest bang for your buck and potentially turnaround a struggling business.

Finally, you need to focus on my one key measure of financial performance. In my view, this is Return on Capital Employed (ROCE). Understand how much capital you have invested in your business and focus on deriving an acceptable return on that.

If your ROCE is not acceptable, you’ll know where to focus your attention.

The answer is usually there somewhere. You just need to know where to look.

Often business owners let their heart rule their head but unless they remember that they also have capital invested in the business and act in a mercenary way, they could end up with a broken heart and zero capital.

If you would benefit from support for your struggling business, we have a number of specialist business advisors who can help with business benchmarking, business growth and business funding. Contact us today for a coffee and an informal chat.