Subscribe for Our Latest Resources

"*" indicates required fields

The State Government has provided multiple forms of land tax relief to landlords through the following measures:

The deferral and waiver will be automatically applied, however, you will need to apply for the rebate.

To be eligible you must fit into one of the two following criteria:

1. You are a landlord who leases a property to one or more tenants and all the following apply:

– Your regular rental income amount is affected by COVID-19.

– You will provide rent relief to the affected tenants.

– You will comply with the leasing principles.

2. You are a landlord and all of the following apply:

– Your property is available for lease.

– Your ability to secure tenants has been affected by COVID-19.

– You require relief to meet financial obligations.

– You will comply with the leasing principles.

More information surrounding the leasing principles can be found at: https://www.treasury.qld.gov. au/budget-and-financial- management/revenue-and- taxation/leasing-principles/

If you would like more information on how to apply please contact a member of the MGI South Queensland team.

The Government has now passed legislation to allow the implementation of the JobKeeper payments to employers and other eligible participants. If eligible, the Government will pay a wage subsidy of $1,500 per eligible employee. The payments will be taxable to the employers and tax-deductible when paid to employees as wages.

JobKeeper will essentially be based on fortnights between 30 March 2020 to 27 September 2020. Called “Jobkeeper fortnights”

In order to assess if you are eligible you need to work through the following criteria:

If you are carrying on a business on 1 March 2020, or are a non-profit body that pursued its objectives principally in Australia on 1 March 2020 you will qualify provided:

a) Your entity satisfies the “decline in turnover test” at or before the time it qualifies for the job keeper payments. The relevant thresholds are as follows:

The decline in projected GST turnover applies to either:

a) A calendar month that ends after 30 March 2020 and before 1 October 2020;or

b) A quarter that starts on 1 April 2020 or 1 July 2020.

As compared with the corresponding period in 2019.

GST turnover includes taxable supplies and GST free sales but excludes input taxed supplies.

You can apply to the ATO for commissioner discretion if you believe this is not an appropriate comparison period.

Example

Patrick Enterprises assesses its eligibility for JobKeeper payments on 6 April 2020 based on a projected GST turnover for April 2020 of $6 million. It considers that the comparable period is the month of April 2019 for which it had a current GST turnover of $10 million. The April 2020 turnover falls short of the April 2019 turnover by $4 million, which is 40% of the April 2019 turnover. This exceeds the specified percentage, so the decline in turnover test is satisfied.

2. Who are eligible employees?

An individual is an eligible employee of an entity for a fortnight if on 1 March 2020:

(a) the individual was aged 16 years or over; and

(b) the individual was:

(i) an employee (other than a casual employee) of the entity; or

(ii) a long term casual employee of the entity (with more than 12 months of regular and systematic employment); and

(c) the individual:

(i) was an Australian resident (within the meaning of section 7 of the Social Security Act 1991); or

(ii) was a resident of Australia for the purposes of the Income Tax Assessment Act 1936 and was the holder of a special category visa referred to in the regulations under the Migration Act 1958 as a Subclass 444 (Special Category) visa.

An individual is excluded from being an eligible employee of an entity for a fortnight if:

(a) parental leave pay is payable to the individual and the individual’s PPL period overlaps with, or includes, the fortnight; or

(b) at any time during the fortnight, the individual is paid dad and partner pay; or

(c) all of the following apply:

(i) the individual is totally incapacitated for work throughout the fortnight;

(ii) an amount is payable to the individual under, or in accordance with, an Australian workers’ compensation law in respect of the individual’s total incapacity for work;

(iii) the amount is payable in respect of a period that overlaps with, or includes, the fortnight.

You must also notify your employee that you have applied for JobKeeper payments on their behalf within 7 days of informing the ATO. Attached is a form that both you and your employee needs to sign for ATO records. We also recommend that you get the employee to sign an acknowledgement and confirm they are not receiving JobKeepeer from any other employer. You must notify the ATO if an employee informs you that you are not their primary employer.

You are not required to notify employees who are not eligible, but you can do so if you wish. Please see the appendix for sample notification and acknowledgement letters.

As an employer you are also not obligated to participate in the JobKeeper program.

3. Do you satisfy the wage condition?

An employer satisfies the wages condition for an Individual for a fortnight if the sum of the amounts paid is equal to or exceeds $1,500 in wages, salary, commissions, bonuses or allowances. These amounts must be subject to withholding.

Employers can elect to top up employees on low incomes to meet the fortnight threshold in order to make the employees eligible. Employers will not be required to pay super guarantee on the top up amounts. However, you can if you like.

4. Have you elected to participate?

If you are eligible to participate you need to notify the ATO of your eligible employees and their details before the end of the relevant fortnight. For the first and second fortnights you will need to notify the ATO prior to the 26 April 2020.

5. What are my ongoing obligations

The employer must report its monthly GST turnover and projected turnover for the following month within 7 days of the end of each month. Therefore the first report will be due on the 7th May 2020.

The ATO will then pay the JobKeeper payment of $1,500 per eligible employee per eligible fortnight not later than 14 days after the end of the calendar month. Therefore the first payment shall be due around the 14th May 2020.

6. Am I eligible for the payment as a business owner?

If your business qualifies for the JobKeeper payment you will also be able to nominate one “eligible business participant” per fortnight to receive an additional $1,500. Eligible business participants cannot be eligible employees of other entities and must be actively engaged in the business conducted by the entity. Eligible business participants must be an individual who is also one of the following:

An entity is not entitled to a JobKeeper payment unless the entity had an ABN on 12 March 2020 and the entity

a) Carried on a business during the 2019 financial year and had lodged its tax return prior to 12 March 2020. Or

b) The entity made a taxable supply between 1 July 2018 and 12 March 2020 and lodge the appropriate activity statement by 12 March 2020.

7. What if my decline in turnover is not what I thought it would be?

There is the risk that you might assume your decline in turnover will be more than the relevant thresholds however it is actually less. If this is the case you might have to pay the JobKeeper payments back to the ATO plus interest. There will be some tolerance if the fall in turnover is slightly less than the relevant decline in turnover percentage. We would urge you to keep records on how you estimated the projected turnover.

Appendix A – Notify Employee eligible for JobKeeper

To: All Eligible Employees

Re: JobKeeper Payment

Date:

______________________________________________________________________________________________________________

The Federal Government has recently introduced legislation confirming a new JobKeeper subsidy. The JobKeeper subsidy is a payment that assists eligible employers impacted by COVID-19 to continue to pay eligible employees.

Eligible employers can claim a payment of $1,500 per fortnight per eligible employee from 30 March 2020, for a maximum period of 6 months.

This memorandum is to confirm that { INSERT COMPANY NAME } will be participating in the JobKeeper scheme. This will allow us to continue to operate our business throughout this crisis, and in turn, keep our employees in jobs as much as possible.

We have nominated you as an eligible employee under the JobKeeper scheme. This means that {INSERT COMPANY NAME } will receive a payment of $1,500 per fortnight from the Government to subsidise your wages.

Employees still working

If you are still working, you will be paid your normal wages based on the hours you work. If you typically receive less than $1,500 before tax per fortnight, you will still be paid the full amount of $1,500 per fortnight, before tax. If you typically receive more than $1,500 before tax per fortnight, you will still receive your normal wages.

Employees on stand down

If you have been stood down, you will be paid $1,500 per fortnight before tax, even if you typically earn less than $1,500 per fortnight. If you typically earn more than $1,500 before tax, you will not be paid over and above the $1,500 JobKeeper payment.

For more information on the JobKeeper subsidy, please see the Treasury website at https://treasury.gov.au/coronavirus/jobkeeper.

If you have any further questions or concerns in relation to this matter, please contact _______ on _________ .

ACKNOWLEDGEMENT

I __________________________________________ (please print name) hereby acknowledge that I have received, read and understand the details confirmed in this memorandum regarding the JobKeeper arrangement, and agree to be an eligible employee for the purposes of the JobKeeper scheme. I also understand that all contents of this letter are private and confidential.

| Signed: | _____________________ |

| Dated: | _____________________ |

Appendix B – Notify employee not eligible for JobKeeper Payment

To:

Re: JobKeeper Payment

Date:

______________________________________________________________________________________________________________

The Federal Government has recently introduced legislation confirming a new JobKeeper subsidy. The JobKeeper subsidy is a payment that assists eligible employers impacted by COVID-19 to continue to pay eligible employees.

Eligible employers can claim a payment of $1,500 per fortnight per eligible employee from 30 March 2020, for a maximum period of 6 months.

This memorandum is to confirm that { INSERT COMPANY NAME } will be participating in the JobKeeper scheme. This will allow us to continue to operate our business throughout this crisis, and in turn, keep our employees in jobs as much as possible.

Unfortunately, you do not meet the eligibility criteria for { INSERT COMPANY NAME } to claim the JobKeeper payment to subsidise your wages. We appreciate that this may result in further financial hardship for you and as such we encourage you, if you have not already, to contact Services Australia about your individual circumstances and to discuss whether you would be eligible for JobSeeker payments.

As the JobKeeper subsidy is available to businesses for a period of six months until 27 September 2020,

{ INSERT COMPANY NAME } will continue to assess your eligibility for this subsidy and will keep you fully informed of any changes that may affect your eligibility as soon as possible.

We would like to take the opportunity to thank you for your continued patience and loyalty during this difficult time.

For more information on the JobKeeper subsidy, please see the Treasury website at https://treasury.gov.au/coronavirus/jobkeeper.

If you have any further questions or concerns in relation to this matter, please contact __________ on ___________ .

ACKNOWLEDGEMENT

I __________________________________________ (please print name) hereby acknowledge that I have received, read and understand the details confirmed in this memorandum regarding the JobKeeper arrangement. I also understand that all contents of this letter are private and confidential.

| Signed: | _____________________ |

| Dated: | _____________________ |

Appendix C – Employer not participating in JobKeeper Program

To: All Employees

Re: JobKeeper Payment – Non-Participation

Date:

______________________________________________________________________________________________________________

The Federal Government has recently introduced legislation confirming a new JobKeeper subsidy. The JobKeeper subsidy is a payment that assists eligible employers impacted by COVID-19 to continue to pay eligible employees.

Eligible employers can claim a payment of $1,500 per fortnight per eligible employee from 30 March 2020, for a maximum period of 6 months.

This memorandum is to confirm that whilst our business may be deemed eligible to participate in the scheme, due to the unprecedented and significant cost COVID-19 has had on our operations and subsequent cashflow, we have made the difficult decision to not participate in this scheme at this time. As a result, we will not be receiving the JobKeeper payments from the Government.

As the JobKeeper subsidy is available to businesses for a period of six months until 27 September 2020, we will notify you if our ability to participate in the subsidy changes.

We encourage all employees to contact Services Australia about their individual circumstances and to discuss whether they are eligible for JobSeeker payments.

We would like to take the opportunity to thank you for your continued patience and loyalty during this difficult time.

For more information on the JobKeeper subsidy, please see the Treasury website at https://treasury.gov.au/coronavirus/jobkeeper.

If you have any questions or concerns in relation to this matter, please contact ___________ on ____________ .

A large number of Australian businesses now require most, if not all of their employees to work from home. As a result, the Australian Taxation Office (ATO) has given workers a simpler way to claim tax deductions working from home. The new announcement allows individuals to claim a rate of 80 cents per hour for all running expenses while working from home, instead of needing to calculate costs for specific running expenses. This is up from 52 cents previously.

This claim is for heating, cooling, lighting, cleaning and so on. The usual substantiation requirements are still in place – for example, you need to have evidence (e.g. a diary) of the hours you worked from home.

Currently, one needs to have a dedicated “work from home area” at home (e.g. a home office) to make working from home claims. This requirement is also removed. The ATO also said multiple people living in the same home can all make individual claims using the 80 cents per hour rate.

The new arrangement only applies to expenses incurred after March 1, 2020, and individuals can still choose to make a working from home claim under existing arrangements that involve calculating all or part of their running expenses. Please contact us if you would like to know more about this method as it may still result in a higher claim depending on your personal circumstances.

There is not yet an end date on the new arrangement but the ATO says it will review it in the next (2021) financial year.

Don’t forget also there are other expenses that can still be claimed in addition to the above, such as decline in value of office equipment, Internet connection, cost of software purchased for work and mobile phone usage. Mobile phone usage is also subject to some administrative short-cuts with a standard $50 fixed deduction per year being allowed. Otherwise, an apportioned deduction based on actual expenses is required – and that can be quite rigorous, requiring a diary to be kept for a representative 4-week period.

Please contact your MGI advisor if you are unsure what you may be entitled to claim.

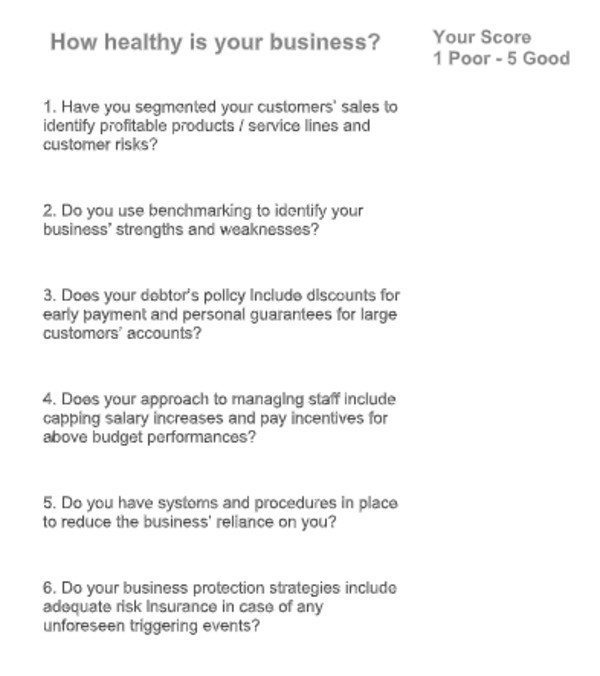

It’s been some time since you started your business. Many business owners have mixed emotions as they experience the highs and lows of owning and running a small business. Very few small business owners take the time to sit back and analyse the changes taking place in their business and business operating environment and then consider how these changes impact on their current and future business situation. Developing business survival strategies is a key part of helping your business to evolve and navigate the ever-changing landscape.

Consider how any or all of the following impact on your business:

Small business owners need to continually evolve the way they do business if they are to survive and thrive. Completing a business SWOT analysis is an essential first step in any effective business planning process with the aim of successfully evolving the business to counter existing weaknesses and threats, bolster strengths and take advantage of opportunities as they arise.

Successful small business owners are able to spend less time working in their business, with more time spent planning their future and developing business survival strategies. Take the time to find out what’s happening in your industry, how you compare with your peers (business benchmarking) and establish a picture of what your business will look like in the future. Invest in planning days with your most trusted Advisers (Accountant and Financial Adviser) so you can get independent and objective advice on how your business is performing.

Are you doing any or all of the following?

How you plan for change will improve your chances of surviving and thriving. Developing business survival strategies doesn’t mean you believe you are going to fail. It means you are giving your business the best chance of growing.

The team at MGI South Queensland have helped many businesses not only survive but thrive through difficult times. We have business coaches as well as experts in tax and risk management. Our outsourced CFO and financial management service gives you access to specialist support who can help you improve your financial procedures and improve your bottom line. Give us a call on 07 3002 4800 or book a consultation online today.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Readers of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. MGI accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

One of the biggest small business risks can often start with the owner! In our many years of working with business owners, it’s not uncommon to hear the following:

“My customers will be with me until the day I die”.

“My business is my identity”.

“My business is my superannuation”.

If you agree with these sentiments, it is likely that your business is overly reliant on you.

You might ask, so what?

A business that relies heavily on its owner is not as valuable as a business that is not reliant on its owner. When we talk about small business risks, many business owners don’t understand the risks of key person reliance and how it can significantly impact the value of their business.

Compare the following valuation scenario of the same business when key person reliance is reduced or minimised:

| Business Key Person Reliant | Same Business not Key Person Reliant | |

| Business Profit | $200,000 | $200,000 |

| Business Valuation Multiple | 3.05 | 3.5 |

| Business Value | $610,000 | $700,000 |

| Value Improvement | $90,000 | |

| Improvement % | 14.75% |

Buyers will pay a higher price for a business that can be easily integrated into their current business or smoothly transitioned to a new principal. They will want some comfort that the business’ key customers and staff will stay with the business once the current owner departs.

There are many different business and risk management strategies business owners can implement to reduce or minimise key person reliance.

The table below provides some suggested examples:

| STRATEGIES | ACTION | |

| Business |

|

1. Business Systems: introduce systems into your business. For example, a good quality stock management system will reduce reliance on the owner’s product and services knowledge. 2. Client Relationship Management: establish customer relationship management protocols so staff can manage key customer relationships. 3. Management Succession: invest in the professional development of your key staff so they can eventually share in part ownership (succession planning) of the business. |

| Risk Management | The very nature of some businesses means it is difficult if not impossible to reduce or remove key person reliance. A specialist surgeon is an example of an occupation that will always be key person reliant. In this case where key person reliance cannot be removed or reduced the purchase of business insurance is considered an effective risk management strategy. |

Start assessing the impact of key person dependency on your business by requesting a business valuation from your accountant. Your accountant is best positioned to provide advice on key person reliance, business valuation and business and risk management strategies to reduce, remove or minimise the risk from key person reliance.

The team at MGI South Queensland can help you with all aspects of improving your business valuation as well as exit planning strategies and business benchmarking for business growth. Our succession planning services will help you make calm and considered decisions about the long term future of your business. Give us a call on 07 3002 4800 or book a consultation online today.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Readers of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. MGI accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

For business owners, running a successful business is often challenging enough, but for many succeeding in business in tough times becomes even harder. What makes the difference between why businesses succeed and fail, particularly in a tough economic environment? Managing through difficult times is an uphill struggle for sure. However, there is good news: there are a few simple measures you can implement to improve the probability that your business will succeed even when the going gets tough.

Often the factors that lead to success in a business come down to some basic but fundamental principles of business management. Implementing these four tips could make the difference between why businesses succeed and fail when the economic environment takes a downward turn.

Contact your key customers and ask them how their business is faring. Meet regularly with high-value customers and offer your support. Understanding their situation means you will be better informed about what you can do to assist them and thus protect and potentially grow your business’ revenue. To grow your own revenue, invest in new innovative (low cost) sales strategies, increase (low cost) sales. Develop marketing strategies and show leadership by spending more time with your customers and sales team.

A reduction in revenue and/or profit means you will need to examine your cost structure to maintain your profitability. Be prepared to make some hard decisions. Low fixed and high variable cost is the ideal cost structure for doing business in tough times.

Non Trading Costs – try to reduce or eliminate non-trading costs. For example, examine wage productivity reports and restructure non-productive roles or encourage multi-skilling to maximise your employee return per hour. Staff reduction is not necessarily a given in tough times!

Variable Costs – examine all your expenses and investigate ways to transfer your business’s fixed costs to variable costs. Outsourcing is a variable cost strategy.

Collecting cash from your customers may become more difficult. Avoid business cash flow problems and consider amending your policies for debtor collection and stock management.

Debtors Collection: place tighter limits on the amount of credit you extend to your customers. If you have exposure to large customers, seek assurances and guarantees on how they will pay their account. Enter repayment schedules and offer ‘cash only’ terms until your customer accounts are in order. If the decision is between being flexible and survival there is really only one choice.

Stock Management: don’t over-invest in stock. Place strict controls over stock ordering and management. If customer sales slow down so should your ordering.

When looking at why businesses succeed and fail in difficult times, it is important you move quickly to minimise your business risk. The first step is to re-examine or develop a new Business Strategy or Plan to review and assess your current situation and plan the future. When preparing your Business Strategic Plan seek guidance from your accountant who is best positioned to provide this advice. Seeking advice early will mean the difference between your business thriving or simply surviving.

The team at MGI South Queensland have helped many businesses not only survive but thrive through difficult times. We have business coaches as well as experts in tax and risk management. Our outsourced CFO and financial management service gives you access to specialist support who can help you improve your financial procedures and improve your bottom line. Give us a call on 07 3002 4800 or book a consultation online today.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Readers of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. MGI accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

Did you ever ask yourself this question during any stage of your practice career? Long gone are the days of starting a business out on a limb and hoping for the best, with the release of Royal Australian College of General Practitioners (RACGP) 5th Edition, a business plan is listed as one of the new standards required.

Indicators in the RACGP Standards 5th edition provides the following guidance on business planning:

Criterion C3.1A – Our practice plans and sets goals aimed at improving our services.

You must:

You could:

Criterion C3.1B – Our practice evaluates its progress towards achieving its goals.

You could:

Whether you are just starting out in a new practice or other stages of the practice life cycle, establishing a business plan is not merely for meeting the new RACGP Standards 5th edition requirement but is critical to achieve your business goals.

Whilst the initial phase of developing a business plan can be overwhelming, a well-developed business plan will set the roadmap of the business progression and guide/support the operational success of a practice.

We have listed some top tips for you to consider before you embark on the journey of developing a business plan.

With extensive experience in helping medical and dental practices to thrive, the team at MGI South Queensland can help you with your existing plan or the development of a business plan to concrete your roadmap to success.

So you are thinking of setting up a not-for-profit organisation and not sure what legal structure to utilise? Or you have an established Non Profit organisation but not sure if your current legal structure is the most effective for you to achieve your NFP purpose? In this blog, we explore the two most common legal structures for NFP organisations in Australia: Non profit Company Limited by Guarantee and Incorporated Associations, and highlight the pros and cons of each option.

The two most popular forms of incorporated structures are Incorporated Associations (IAs) and Non Profit Company Limited by Guarantee (CLG). In a number of cases, entities may start out as IAs but will later restructure themselves as CLGs as their operations and needs change.

Choosing the right incorporated structure for your organisation is a very important legal decision, as it has consequences for:

Incorporated Associations were introduced as a legal structure to provide a simple and inexpensive means of incorporating not-for-profit groups. All States and Territories have their own, slightly different, laws to set up associations.

IAs can only operate within the State that they are registered – so for Queensland under the Associations Incorporation Act 1981 (Qld), an IA can only have operations within the QLD state boundaries. If your NFP has, or is planning operations in multiple states (including fundraising in other states, e.g via a nationwide internet appeal), then an IA model is unlikely to be appropriate to meet your needs.

The Government Regulator of IAs in QLD is the Office of Fair Trading. If you are registered as a charity, you will also be registered with the Australian Charities and Not-for-profit Commission (ACNC), and must also report to the ACNC. This means IAs that are registered charities will report to at least two regulators.

Reporting and audit requirements are on a tiered basis, with tier 1 IAs (current assets or revenue greater than $100k) having a requirement to prepare financial statements and have them audited.

Tier 2 IAs (current assets or revenue between $20,000 and $100,000) have a requirement to prepare financial statements, have them signed by an approved person who can certify that financial records show that the IA has adequately controls in place. These financials are also required to be lodged with the Office of Fair Trading, but no requirement for an audit.

Tier 3 IAs are also required to lodge financial statements, with the IA’s President or Treasurer preparing a signed statement stating that the IA keeps financial records in a way that properly records the association’s income and expenditure and dealings with its assets and liabilities.

There is no requirement for the accounts to be audited or reviewed.

Although we often think of a ‘company’ as being a business, a non profit Company Limited by Guarantee (‘CLG’) is a special type of company structure for not-for-profit groups all across Australia. Just like a business company, it has ‘directors’, but unlike a business, has ‘members’ instead of ‘shareholders’. Some of the provisions of the Corporations Act (eg. directors’ duties and penalties) that apply to ‘for-profit’ companies also apply to CLGs.

This structure is most commonly used for NFPs wanting to operate across Australia (or in multiple states), or larger NFPs, including those that only operate in one state.

Some legislation requires the non profit Company Limited by Guarantee structure for certain types of organisations (eg. registered housing and aged care providers). A CLG structure is also suitable for a wholly owned subsidiary organisation, as it can be set up with just one member (but does need to have three directors).

The Government Regulator of CLGs for registered charities is the ACNC, but certain Corporations Act 2001 regulations still apply to registered charities.

If a CLG is not a registered charity, but still meets the definition of a NFP entity, then currently this type of non profit Company Limited by Guarantee is still regulated under the Corporations Act 2001 and is required to lodge financial statements with ASIC. This may change in the future as the ACNC extends its coverage across NFPs in Australia.

Reporting and audit requirements are again on a tiered basis, with either a large, medium or small charity ranking under the ACNC.

ACNC CLGs with revenue greater than $1M per annum are classified as a large charity requiring a full audit and lodgement of financial statements with the ACNC.

ACNC CLGs with revenue between $250,000 and $1M per annum are classified as medium sized charities and can adopt to have a ‘review’ rather than a full audit, which provides a lower level of assurance from the auditor. Financial statements must be lodged with the ACNC.

ACNC CLGs with revenue less than $250,000 are classified as small sized charities, and can choose whether to submit financial statements to the ACNC. No review or audit is required.

All sized ACNC CLGs are required to lodge an Annual Information Statement with the ACNC annually.

CLGs that meet the definition of a not-for-profit but that are not a registered charity currently still lodge financial statements with ASIC.

If the CLG has turnover of greater than $1M per annum, an audit is required. If the CLG has a turnover of less than $1M per annum, a review is required to be performed.

Generally speaking, if your NFP is only operating in one State and is not deemed to be a large (*) not-for-profit, then an IA model may be an appropriate structure for your organisation.

N.B.(*) ‘Large’ in this sense is generally accepted to follow the tiered classifications under the ACNC Act 2012– e.g revenue greater than $1M.

However, if your NFP is operating in multiple States across Australia, and/or your organisation is of a larger size, the CLG model may be a more appropriate structure for your organisation.

Other benefits of considering a move to a CLG include:

Any decisions to adopt/change your NFP structure should be run past a qualified not for profit legal advisor who can consider your organisation’s specific circumstances.

If you are operating an IA and are considering changing to a CLG structure, the transition may be simpler than you think. Organisations can now transfer directly to a CLG from an IA, subject to passing a special resolution of members and being approved by ASIC.

There may be tax consequences of doing so (for example – stamp duty) – so it is advised to consult a qualified NFP accountant to discuss.

A number of factors will influence an organisation’s decision about whether to become an IA or a CLG. There is no quick and easy answer, but weighing up the various factors will help you to determine which structure best suits the activities, circumstances, direction and resources of your particular group.

MGI South Queensland are not for profit accounting and audit specialists. If you would like to find out more about Non Profit Company Limited By Guarantee or Incorporated Association structures, contact us today on 07 3002 4800 today and let us shout you a coffee to discuss your requirements..