Subscribe for Our Latest Resources

"*" indicates required fields

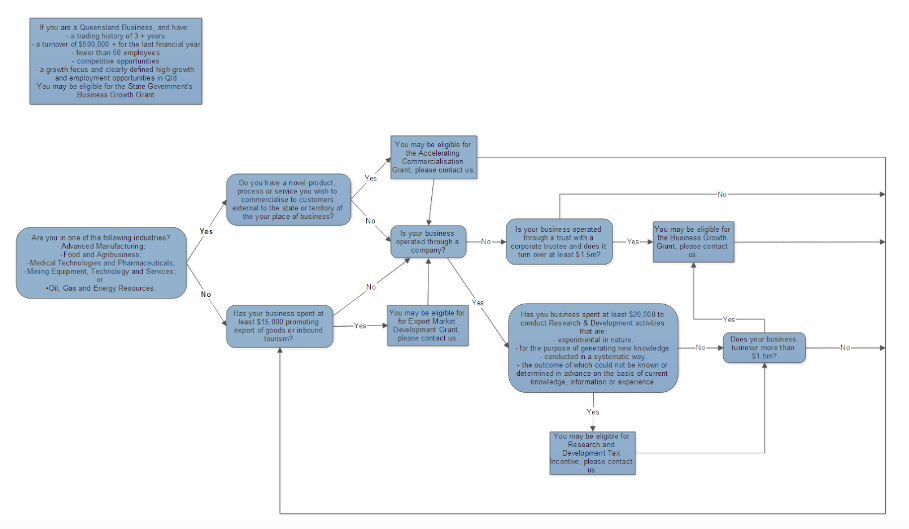

The Queensland government has introduced a Business Boost grants program which is aimed at providing support to businesses to advance improvements in their efficiency and productivity with funding of up to $15,000 (excluding GST) on meeting the criteria.

This grant supports activities in 3 project areas:

To be eligible for the grant, the business must (at the time of applying):

Your business may be eligible to receive a grant payment of up to $15,000 (excluding GST) on completing your proposed project.

The successful applicants must co-contribute at least 30% of the total project costs.

Grant funding will be paid only after compliant acquittal documentation is received.

Grant funding is not eligible to projects with a total cost of less than $10,715 (excluding GST) and payments made before the approval date.

Applications open at 9am on 30 July 2021. The application form will be available online after this date via the DTESB SmartyGrants portal.

https://dtesb.smartygrants.com.au/

This grant program is competitively assessed and not all applications will be funded.

Our team will be available to assist you to maximise your chance of receiving the grant.

It’s been some time since you started your business. Many business owners have mixed emotions as they experience the highs and lows of owning and running a small business. Very few small business owners take the time to sit back and analyse the changes taking place in their business and business operating environment and then consider how these changes impact on their current and future business situation. Developing business survival strategies is a key part of helping your business to evolve and navigate the ever-changing landscape.

Consider how any or all of the following impact on your business:

Small business owners need to continually evolve the way they do business if they are to survive and thrive. Completing a business SWOT analysis is an essential first step in any effective business planning process with the aim of successfully evolving the business to counter existing weaknesses and threats, bolster strengths and take advantage of opportunities as they arise.

Successful small business owners are able to spend less time working in their business, with more time spent planning their future and developing business survival strategies. Take the time to find out what’s happening in your industry, how you compare with your peers (business benchmarking) and establish a picture of what your business will look like in the future. Invest in planning days with your most trusted Advisers (Accountant and Financial Adviser) so you can get independent and objective advice on how your business is performing.

Are you doing any or all of the following?

How you plan for change will improve your chances of surviving and thriving. Developing business survival strategies doesn’t mean you believe you are going to fail. It means you are giving your business the best chance of growing.

The team at MGI South Queensland have helped many businesses not only survive but thrive through difficult times. We have business coaches as well as experts in tax and risk management. Our outsourced CFO and financial management service gives you access to specialist support who can help you improve your financial procedures and improve your bottom line. Give us a call on 07 3002 4800 or book a consultation online today.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Readers of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. MGI accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

For business owners, running a successful business is often challenging enough, but for many succeeding in business in tough times becomes even harder. What makes the difference between why businesses succeed and fail, particularly in a tough economic environment? Managing through difficult times is an uphill struggle for sure. However, there is good news: there are a few simple measures you can implement to improve the probability that your business will succeed even when the going gets tough.

Often the factors that lead to success in a business come down to some basic but fundamental principles of business management. Implementing these four tips could make the difference between why businesses succeed and fail when the economic environment takes a downward turn.

Contact your key customers and ask them how their business is faring. Meet regularly with high-value customers and offer your support. Understanding their situation means you will be better informed about what you can do to assist them and thus protect and potentially grow your business’ revenue. To grow your own revenue, invest in new innovative (low cost) sales strategies, increase (low cost) sales. Develop marketing strategies and show leadership by spending more time with your customers and sales team.

A reduction in revenue and/or profit means you will need to examine your cost structure to maintain your profitability. Be prepared to make some hard decisions. Low fixed and high variable cost is the ideal cost structure for doing business in tough times.

Non Trading Costs – try to reduce or eliminate non-trading costs. For example, examine wage productivity reports and restructure non-productive roles or encourage multi-skilling to maximise your employee return per hour. Staff reduction is not necessarily a given in tough times!

Variable Costs – examine all your expenses and investigate ways to transfer your business’s fixed costs to variable costs. Outsourcing is a variable cost strategy.

Collecting cash from your customers may become more difficult. Avoid business cash flow problems and consider amending your policies for debtor collection and stock management.

Debtors Collection: place tighter limits on the amount of credit you extend to your customers. If you have exposure to large customers, seek assurances and guarantees on how they will pay their account. Enter repayment schedules and offer ‘cash only’ terms until your customer accounts are in order. If the decision is between being flexible and survival there is really only one choice.

Stock Management: don’t over-invest in stock. Place strict controls over stock ordering and management. If customer sales slow down so should your ordering.

When looking at why businesses succeed and fail in difficult times, it is important you move quickly to minimise your business risk. The first step is to re-examine or develop a new Business Strategy or Plan to review and assess your current situation and plan the future. When preparing your Business Strategic Plan seek guidance from your accountant who is best positioned to provide this advice. Seeking advice early will mean the difference between your business thriving or simply surviving.

The team at MGI South Queensland have helped many businesses not only survive but thrive through difficult times. We have business coaches as well as experts in tax and risk management. Our outsourced CFO and financial management service gives you access to specialist support who can help you improve your financial procedures and improve your bottom line. Give us a call on 07 3002 4800 or book a consultation online today.

Disclaimer: this information is of a general nature and should not be viewed as representing financial advice. Readers of this information are encouraged to seek further advice if they are unclear as to the meaning of anything contained in this article. MGI accepts no responsibility for any loss suffered as a result of any party using or relying on this article.

Did you ever ask yourself this question during any stage of your practice career? Long gone are the days of starting a business out on a limb and hoping for the best, with the release of Royal Australian College of General Practitioners (RACGP) 5th Edition, a business plan is listed as one of the new standards required.

Indicators in the RACGP Standards 5th edition provides the following guidance on business planning:

Criterion C3.1A – Our practice plans and sets goals aimed at improving our services.

You must:

You could:

Criterion C3.1B – Our practice evaluates its progress towards achieving its goals.

You could:

Whether you are just starting out in a new practice or other stages of the practice life cycle, establishing a business plan is not merely for meeting the new RACGP Standards 5th edition requirement but is critical to achieve your business goals.

Whilst the initial phase of developing a business plan can be overwhelming, a well-developed business plan will set the roadmap of the business progression and guide/support the operational success of a practice.

We have listed some top tips for you to consider before you embark on the journey of developing a business plan.

With extensive experience in helping medical and dental practices to thrive, the team at MGI South Queensland can help you with your existing plan or the development of a business plan to concrete your roadmap to success.

Holding more stock than you need is never a good idea. Excess stock can literally be dead money taking up space and locking up your cash flow. As interest rates increase it can also be very expensive to fund.

While funding has been accessible and rates low, it can lull businesses into a false sense of security that they can perhaps take advantage of a “good deal” and stock up while the price is right etc. This kind of thinking can however lead to disaster as your free cash flow dries up and interest rates start to rise.

You would have no doubt heard of lean manufacturing and “just in time” ordering in the manufacturing environment. This concept is to have just enough stock for the production cycle at any point in time and no excess. This keeps your cash requirements in stock low. The just in time theory may not always be as easily applied in other environments where say items need to be imported or there is a long lead time etc from your supplier, it is something that you should think about applying to your business.

Advisers and accountants often talk about your “inventory turn” in terms of your business operating cycle. Inventory turn is the number of times in a year your inventory is completely turned over. If say, your cost of goods sold is $500,000 and you hold $100,000 in stock, your turn rate is 5 times. From a business management perspective the higher the rate of inventory, turn the lower the amount that you have invested in inventories and therefore the lower the risks for your business. It is therefore an important that you have a goal of maximum inventory turns. It will free up your cash and free up your warehouse!

You will need to consider your buying patterns. You obviously need to have enough stock to meet customer demand, so give thought to lead times on products. Is it possible to order less more frequently?

Although volume discounts and shipping costs can mean the price per unit may increase if you are ordering smaller quantities you will need to compare this to the cost of holding that stock for longer than you need to. There is the financing cost, the warehouse storage space being occupied as well as the opportunity cost of what you might be able to do with your money if it wasn’t tied up in stock.

Understanding your sales patterns comes from having good data and systems to track which customers are buying which items, when and in what quantities. This information is critical in you setting your buying strategy.

Make sure you know where your stock is. Organise it so that it is accessible and visible when you need it. You don’t want to be in a situation where your inventory management system is saying you have items in stock but you can’t find them when your customers want them or even worse “mystery” boxes of stock popping up and surprising you. You can’t sell what you don’t know you have. Good organisation of your storage area will keep things in plain sight and at hand when needed.

You should also consider investing in good inventory tracking software or add-ons to your accounting system. This will streamline your stock takes and keep the information you need about your stock holdings at your fingertips. There are quite literally a myriad of different stock management applications that can integrate to your general ledger, online store, point of sales and other systems. Speak to your adviser about how to select the best option for you and your business.

Supplier terms of trade will also be important in your buying strategy. Looking at credit terms that suppliers offer, it is a low cost tool in funding your inventory.

As we move more to the digital marketplace and online shopping small businesses might also find it easier to purchase goods direct online. This will generally mean that payment is required before the goods ship. Again, you may be able to source a better per unit price this way but you will need the free cash flow to fund the purchases.

An alternative is to look to more traditional supplier that do offer trading terms. In this case matching your stock orders to the terms offered will help you maximise your cash flow. Ideally, if your suppliers offer 30 day terms you would only order sufficient stock to cover 30 days sales.

Some suppliers may allow terms which are a set number of days after end of month. Where this is the case, consider ordering inventory earlier in the month to maximise the number of days you have available to sell the goods before having to pay for them.

Another really important consideration is the life of the product. Is there a risk that it will be come obsolete before you have the opportunity to sell it or does it have some other “use by” or “best before” date consideration. The longer you hold your stock the higher the risk that you may have to dispose of it before you can sell it.

Slow moving stock is a problem in many businesses. While we all want to maximise our return or profit margin on our stock purchases, sometimes it is best to accept that you may have made the wrong call about some items or that the market has moved and see if you can sell them at a discount before those goods become obsolete.

A good handle on your operating cycle and stock requirements will keep your cash working for you and clear out your storage areas, keeping you focussed on high value sales and services. Whereas a lack of focus on your stock levels can really cost you more than you may realise.