Subscribe for Our Latest Resources

"*" indicates required fields

If you are an employer, you’ll have an extra step to take if you have new employees who start from 1 November 2021 and they don’t choose a super fund.

You may now need to request their ‘stapled super fund’ details from the Australian Tax office (ATO).

A stapled super fund is an existing super account of an employee that follows them as they change jobs.

This change aims to stop your new employees paying extra account fees for unintended super accounts set up when they start a new job.

You may need to request stapled super fund details when:

You may still need to request stapled super fund details for some employees even though you don’t need to offer them a choice of super fund. This includes if your employees are temporary residents or they’re covered by an Enterprise Agreement or Workplace Determination made before 1 January 2021.

You and your representatives can request stapled super fund details for your employees if you have full access to ATO Online services for business (previously called the Business portal) or contact us to complete this step for you. It is important that if you are accessing the information via online services, that you review and update any online accesses to protect the privacy and safety of your employees’ personal information.

You must meet your choice of super fund requirements and any stapled super fund obligations by the quarterly due date or you may face penalties.

Step 1: Offer your eligible employees a choice of super fund

You need to give your eligible new employees a Super standard choice form and pay their super into the account they tell you on the form. Most employees are eligible to choose what fund their super goes into.

There is no change to this step of your super obligations.

Step 2: Request stapled super fund details

If your employee doesn’t choose a super fund, you may need to log into the ATO Online services for businesses and go to ‘Employee Super Accounts’ to request their stapled super fund details or contact us to complete this step for you.

The ATO will provide your employee’s stapled super fund details after they have confirmed that you are their employer.

If the ATO provide a stapled super fund result for your employee, you must pay your employee’s super using the stapled super fund details the ATO provide you.

Step 3: Pay super into a default fund

You can pay into a default fund, or another fund that meets the choice of fund obligations if:

If you have any queries in relation to the above, please contact one of the team at MGI South Qld.

The Fair Work Ombudsman has published a new Casual Employment Information Statement.

The attached is the statement which should be given to all new casual employees when they start work.

Please contact your HR team to understand what this means for your business. Feel free to contact your MGI Adviser should you need a referral to an HR expert.

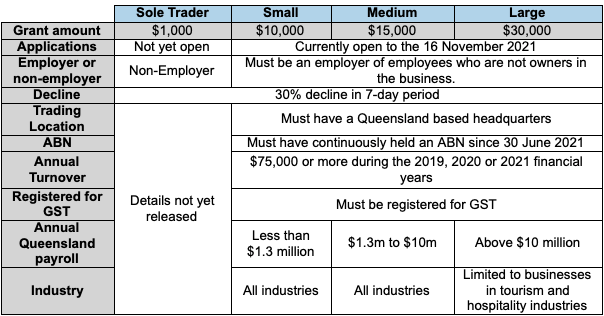

The Queensland government has introduced a Business Boost grants program which is aimed at providing support to businesses to advance improvements in their efficiency and productivity with funding of up to $15,000 (excluding GST) on meeting the criteria.

This grant supports activities in 3 project areas:

To be eligible for the grant, the business must (at the time of applying):

Your business may be eligible to receive a grant payment of up to $15,000 (excluding GST) on completing your proposed project.

The successful applicants must co-contribute at least 30% of the total project costs.

Grant funding will be paid only after compliant acquittal documentation is received.

Grant funding is not eligible to projects with a total cost of less than $10,715 (excluding GST) and payments made before the approval date.

Applications open at 9am on 30 July 2021. The application form will be available online after this date via the DTESB SmartyGrants portal.

https://dtesb.smartygrants.com.au/

This grant program is competitively assessed and not all applications will be funded.

Our team will be available to assist you to maximise your chance of receiving the grant.

Shrinkage in the retail sector has a major impact on the profitability of supermarkets and other stores. Shrinkage is the result of theft by customers and staff, and is also caused by damage to goods as a result of poor ordering and handling practices. It can be equal to three per cent of sales at some independent supermarkets. The shrinkage problem tends to be worse in smaller stores with an average shrinkage factor of around five percent. If retailers want to improve profitability they first need to understand shrinkage.

A recent case study revealed a supermarket business turning over 10 million dollars per year while poor shrinkage control contributed to losses of 10 thousand dollars per week off its bottom line. It seems the smaller a supermarket is, the higher the shrinkage problem. As independent supermarkets increase their turnover, the shrinkage problem reduces to an average of around 1.75 percent. Better quality systems, and better management of the factors that drive shrinkage, contribute to the lower figure in larger supermarkets. Best practice operations are achieving shrinkage levels of less that 0.5 percent.

In reality, most supermarket operators do not know the true cost of shrinkage. Often this is the difference between success and failure of the business particularly when profit margins are so tight. An improvement in shrinkage management of just one per cent of sales can improve profitability by thirty-three percent. This type of saving can enable retailers to channel their resources into areas which will make a positive impact upon their cash flow.

Shrinkage can be defined as the loss in margin due to poor stock management procedures, reporting practices and internal controls. It is measured by comparing the gross margin from the Point of Sale (POS) Report to the financial accounts or internal stock management reports.

Some of the factors that contribute to shrinkage include theft by customers and staff in the supermarket, inconsistent pricing practices, excessive and uncontrolled discounting, absence or infrequent stock taking, as well as damage to goods as a result of poor handling and ordering practices. For managers and owners, shrinkage is a very attractive area to address as the benefits flow straight to the bottom line. We advocate benchmarking the store to identify the gravity of the issue.

Some of the best practice operators have achieved low shrinkage levels by implementing stock management systems, which are compatible to existing POS systems, allowing for automatic re-ordering, regular rolling stock-takes on high-risk items, and stock management procedures. These systems are supported by staff training and job descriptions and assigning responsibility to selected staff, thus delivering tangible benefits to the supermarket owner.

Just some of these benefits include improved cash flow from reduced stock levels, as a result of ordering of stock consistent with sales demand, reduced theft by making high risk items more visible to staff, and providing an early detection of pilferage through instant stock management reporting.

This type of improvement enables the retailer to then direct their resources into other areas, such as improving their supermarket layout and design. Shrinkage efficient supermarkets are most likely to survive and thrive in a competitive market. To improve profitability allows retailers access to funding for supermarket refurbishments, which is an essential part of competing for market share against national chains.

Financial benefits show as soon as a supermarket addresses its shrinkage problem. The best way to begin this process is for the retailer to talk to a professional adviser, or seek advice from industry specialists to develop an action plan to implement better operational practices.

Most retailers are time-poor and work long hours so the most effective way to develop a shrinkage plan is to identify your immediate goals, determine what resources are required (money, people, and time) and allocate tasks to responsible persons. One of the biggest shrinkage issues is that supermarket owners do not compare their management account gross profit (GP) percentage with what comes out from their POS system. This is a big mistake. We found most retailers were unable to produce accurate management accounts on a timely basis and most often conduct stock-takes once a year for tax purposes.

Shrinkage loss really hits home when retailers compare their GP in the financial accounts provided by their Accountant to POS reports. The key is to develop a stock management system that allows for timely and accurate management reporting. Our industry manager recently saw supermarket figures showing a nine percent difference between the POS GP percentage and accounting GP percentage.

For example, regular weekly stock-takes of high wastage and theft items (e.g. meat and fruit/vegetables and tobacco) and cyclic stock-takes on other items will allow for effective monitoring of GP variances.

Adopting a standardised chart of account and journals will improve management reporting of shrinkage as scanning systems ignore the issue. Some supermarket chains have front-end systems that record all customer returns and place the reason for the return and reports at the back office each day and for the week. Further ‘reduced to clear items’ are also all managed via the front end.

Some chains also ensure its cleaners to place floor waste into a separate bin. This separate bin is then checked to see what products the cleaners have swept up and if these products can be reclaimed. It is important that staff take the time to monitor stock, even if it does mean checking the dairy fridge more frequently. You can use technology to keep track of perishables within the supermarket.

The Fair Work Ombudsman has published a new Fair Work Information Statement that incorporates the recent law changes to casual employment.

The attached is the new version which should be given to all new employees.

Please contact your HR team to understand what this means for your business. Feel free to contact your MGI Adviser should you need a referral to an HR expert.