Subscribe for Our Latest Resources

"*" indicates required fields

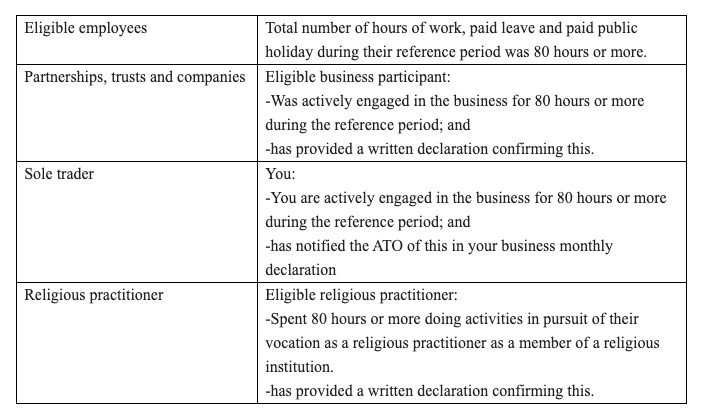

The alternative decline in turnover test for JobKeeper fortnights from 28 September onwards has been released by the ATO.

The new alternative tests are in line with the original covering the 7 circumstances outside the usual business operation that resulted in your 2019 relevant comparison period not being appropriate for applying the basic decline in turnover test.

This includes the following:

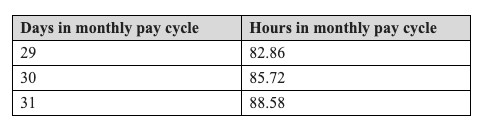

Below are some of the key changes that you should take into consideration when applying the appropriate tests

As with the previous alternative test or the basic decline in turnover tests, you will need to maintain sufficient and appropriate documentation on how the tests have been applied in case of an ATO review.

Please feel free to contact the team at MGI South Queensland if you wish you to discuss the application of the alternative test to your circumstances.

The government has announced that the current $1,500 per fortnight JobKeeper payment will continue past 27 September. However, it will be reduced to $1,200 per fortnight from 28 September, and $750 per fortnight for employees working less than 20 hours a week.

From 4 January, the rate will fall to $1,000 per fortnight and $650 for people working less than 20 hours a week.

Full details of the updated JobKeeper program can be found here.

Businesses looking to remain on JobKeeper beyond 27 September will be required to meet new eligibility tests.

Businesses will still be required to demonstrate the required reduction in turnover i.e. 30 per cent for businesses with turnovers of $1 billion or less, 50 per cent for those with turnover of more than $1 billion, and 15 per cent for ACNC-registered charities.

The current JobKeeper programs requires a business to apply the test for one period (a month or a quarter) prospectively. However, the government will now require businesses to reapply the tests for the June and September quarters to be eligible for JobKeeper beyond September.

In addition, businesses will need to demonstrate that they have met the relevant decline in each of the three quarters ending on 31 December 2020 (June, September and December quarters) to remain eligible for the payment from January 2021 to March 2021.

We will continue to update this post once more details are known.

Please contact your MGI South Queensland advisor should you have any queries.