Subscribe for Our Latest Resources

"*" indicates required fields

The general transfer balance cap is set to increase to $2 million on 1 July 2025, following the release of quarterly CPI data.

With all groups CPI figure reaching 139.4 for the December 2024 quarter, the general transfer balance cap will be indexed for the 2025–26 year, increasing to $2 million from $1.9 million.

The cap limits the amount of money that can be transferred into the retirement phase in super. The increase means clients commencing their first retirement phase income stream in 2025–26 will start with a personal transfer balance cap of $2 million.

Clients who already have a personal transfer balance cap that they have not fully utilised at any time in the past will see their cap increase on 1 July 2025 by a smaller amount due to proportional indexation.

This increase also affects other superannuation rules and concessions including the total superannuation balance, which will also increase to $2 million.

A member’s total super balance at 30 June 2025 will need to be less than $2 million for them to access the standard non-concessional contributions cap.

The 3-year bring forward rule will be limited against a higher Total Superannuation Balance as per below:

To 30 June 2025

From 1 July 2025

If you have any queries or concerns or need further advice and support about superannuation changes please don’t hesitate to reach out to the team at MGI.

When it comes to purchasing an investment property, a big decision you’ll need to make is whether to use super to buy the investment property.

Unfortunately there is no one size fits all answer. It depends on what you are trying to achieve and the resources you have at hand. When it comes to purchasing an investment property, a big decision you’ll need to make is whether to purchase the property inside or outside of super. Unfortunately there is no one size fits all answer. It depends on what you are trying to achieve and the resources you have at hand.

There are much higher set up costs associated with purchasing a property through a self-managed super fund. As an example, you may need to have a combined superannuation balance of at least $200,000 to purchase a property worth approximately $600,000 to cover:

If you can only just scrape together this balance it may not be in your best interest to tie up most of your super in an illiquid asset. Let me explain. Typically a property loan goes for 30 years, so unless you have many working years ahead of you, you’ll need to consider whether you have enough cash left in superannuation to cover pension payments. Secondly superannuation balances can be used to provide a much needed payout should you be diagnosed with a terminal illness. If all your superannuation is tied up in property you will not be able to access this quickly in the event of a terminal illness.

If superannuation is a viable option, the next step is to consider why you are purchasing an investment property and whether purchasing through superannuation will allow you to achieve your objectives. To determine this let’s look at the benefits of using super to buy investment property.

For most of us, superannuation is one of our biggest long-term investments. You may well need to access this to be able to afford the deposit for your investment property. In this case purchasing through super is your only option. However if you have enough cash inside and outside of super then it pays to keep considering the benefits under each.

Especially if you have a high yield property it may be appealing to purchase the property through your superannuation where any income earned will be taxed at 15% rather than your personal tax rate which is generally much higher.

If you plan to hold the asset until your superannuation is in pension phase, you may pay no tax on capital gains if your balance is under the $1.9M transfer balance cap. This can be a significant saving compared to an asset owned outside of superannuation, where you’ll pay tax at your marginal tax rate on the taxable capital gain.

If you don’t hold the asset until retirement you will pay 15% tax on two thirds of the capital gain on a property held for more than 12 months.

If you are looking for additional asset protection superannuation can be a great way to go. Assets held in superannuation are generally protected in a lawsuit and are not at risk of creditors.

Owning an investment property can provide diversification to your investment portfolio, which can help spread risk. This can be particularly useful if your superannuation fund is heavily invested in traditional assets like stocks and bonds.

Property has historically shown the potential for long-term capital growth. This can help your superannuation account grow over time, potentially providing a source of retirement income.

If you are a business owner who is looking to purchase your business premises, superannuation can be a very appealing option. Business premises are generally high yield rental properties. By purchasing the premises in an SMSF business owners can minimise tax paid on rental income and can secure an asset for their retirement without changing their business cash flow.

You can claim interest on a loan to acquire a property in a SMSF, however, the tax benefits here are less because:

– Generally the banks will only loan you 50 – 70% of the purchase price so you will have a smaller loan

– You are only paying 15% tax on superannuation earnings where as you are paying anywhere up to 45% on personal income tax.

Therefore if a property will be significantly negatively geared, and if you have a high personal tax rate, then it is likely that you will achieve a better tax outcome purchasing outside of superannuation. But to make an educated assessment, you would need to “do your numbers” using some assumptions.

There are a number of additional restrictions on how you can use properties held by SMSFs. Firstly you or any fund member’s related parties cannot live in or rent the property. The exception to this is a commercial property which can be used to house a fund member’s business. Also there are restrictions on improving a property that has been acquired by a SMSF using a loan.

The rules governing superannuation investments can change over time. There’s a risk that future changes in regulations could impact your ability to invest in property through your super.

If you borrow to purchase the property within your superannuation fund (using a limited recourse borrowing arrangement or LRBA), you may be exposed to additional risks if the property’s value declines, as you’re still responsible for repaying the loan.

If you use super to buy an investment property, particularly if it is a commercial property, it requires time-consuming paperwork and regular valuations. If ease of investment is a top priority you should think carefully before purchasing property through an SMSF.

At the end of the day whether you should use superannuation to purchase an investment property will come down to what you want to achieve. Superannuation may well present an opportunity to purchase a property that you could not do otherwise. It can also provide tax savings and better asset protection. It is definitely worth having a conversation with an experienced MGI adviser, particularly if you are a business owner, to explore whether you should be looking to at super to fund your next property investment.

Give the team of SMSF Accountants at MGI South Queensland a call or book an appointment for a review of your super strategy today.

This article was first published in December 2017 and has been updated and republished in May 2023.

The content above has been prepared by Accountable Financial Solutions Pty Ltd (“Accountable”), ABN 36 146 520 390. The above information is general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice. Although every effort has been made to verify the accuracy of the information contained above, Accountable, its officers, employees and agents disclaim all liability (except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained on this website or any loss or damage suffered by any person directly or indirectly through relying on this information.

Here is a brief summary of the Federal Budget 2023 updates relevant for individuals:

Superannuation

To get the maximum benefits from the new measures announced in the 2023 Federal Budget, please contact us immediately to book in your 2023 Tax Planning meeting with us. We also have a 2023 Federal Budget overiew for business owners.

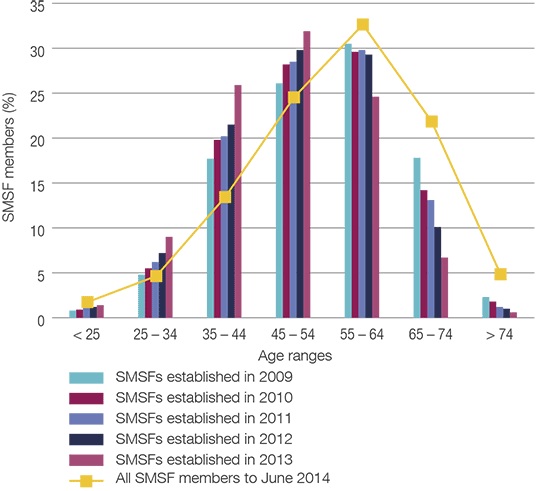

Data recently released by the Australian Tax Office (ATO) confirm that Australians have continued their love affair with self managed superannuation funds (SMSF’s).

The ATO publishes quarterly information about SMSF’s. Here’s a summary:

At 30th September 2021, there were nearly 600,000 (598,452) SMSF’s with just over 1.1m members (1,123,949), averaging 1.87 members per fund. With 53% of male members and 47% of female members, most SMSF’s appear to be your typical “mum and dad” super fund. Just on 70% of SMSF’s are two member funds, around 23% are one member funds, with the balance being three and four member funds.

Based on the most recent data available (2020 year), the average value of a SMSF is around $1.3m, with an average value per member of around $695k. This compares favourably with the average super fund balance of all Australians, which for those aged between 40 and 55, is between $121k and $214k for men and between $92k and $157k for women. (1)

The ATO data indicates that SMSF’s hold more than $860 billion in wealth, with around $29 billion in borrowings and a further $6.7 billion in other liabilities resulting in total net SMSF assets of around $825 billion. So, where is all this money invested?

Well, around $149 billion (or around 18%) is invested in cash and term deposits. A further $238 billion (or around 29%) is invested in listed shares and $53 billion (6%) in listed trusts. A further $134 billion is invested in property, with most of that (around $88 billion) invested in non-residential property.

Interestingly, the proportion of SMSF funds invested in cash and term deposits is highest amongst smaller balance SMSF’s, perhaps reflecting a more conservative approach given the recent volatility in share markets.

Around $63 billion of SMSF wealth was invested in limited recourse borrowing arrangements (LRBA) – basically, assets purchased by SMSF’s using allowable debt. This could be either shares or property. The appetite for LRBA’s appears to be highest in SMSF’s with between $200k and $1m in assets, with an average of around 15% of fund assets comprising LRBA’s.

SMSF trustees have also embraced crypto-currency, with around $230m held in crypto. This has grown steadily since the ATO commenced to measure investments in crypto.

There appears to have also been an increasing appetite for international shares, which now stands at around $12.5 billion.

Interestingly, around half a billion dollars ($509m) is invested in collectables and personal use assets.

In terms of member ages, there is a relatively even distribution between members aged 35 to 84, but relatively small representation from members aged under 35, perhaps indicating the lack of superannuation savings from this age group to be able to justify the establishment of a SMSF.

Interestingly, the 2021 financial year saw a near 20% surge in new SMSF’s established with 25,760 new funds established. However, the number of wind-ups of SMSF’s in 2021 halved from the levels of the previous two years, resulting in a significant increase in the number of net establishments. So it appears that Australian’s love affair with SMSF’s may have longer to run yet.

(ASFA figures as at July 2019).

If you need the support of a specialist SMSF accountant, the team at MGI are here to help.

Last week marked the biggest change to depreciation legislation in 15 years.

As part of the government’s efforts to claw back negative gearing parliament passed the Treasury Laws Amendment (Housing Tax Integrity bill) into legislation.

This legislation means that you can no longer claim income tax depreciation for plant and equipment assets in second-hand properties unless you have personally made the outlay.

This legislation is grandfathered which means if you exchanged contracts prior to 7.30pm on the 9th of May and have previously been claiming tax deductions on the assets you will not be affected.

However for those second-hand properties purchased after 7:30pm on the 9th May you will no longer be eligible to claim these deductions.

Plant and equipment assets are items considered to be easily removable from the property such as air-conditioning, solar panels, blinds and curtains, and carpet.

The good news is there are still a number of opportunities to claim income tax depreciation for investment properties.

New houses are still eligible for deductions on plant and equipment as are properties considered to be substantially renovated by the previous owner.

Plant and equipment assets that have been installed and paid for by you personally will also continue to be income tax depreciable.

Other examples where you will still be able to claim deductions for plant and equipment include:

Investment property owners will also continue to be able to claim for qualifying capital works depreciations. These are considered to be the building’s structure and permanently fixed assets.

If you would like further information on how these changes might impact you contact your MGI advisor. BMT has a helpful tax depreciation calculator if you are considering purchasing a residential investment property in the future and would like to know what tax deductions you might be able to achieve.

A common question that we often get asked by our clients is “How can I protect assets left to my children from in-laws if their marriage breaks down?”

The best way to achieve greater control over the distribution of the assets in your will is to establish a testamentary trust.

A testamentary trust is also highly beneficial when splitting income with young children or where asset protection strategies are required (for instance if a beneficiary is in a high risk occupation).

A testamentary trust is a trust established in a will that comes into effect upon the death of the person making the will. The assets are held in the trust with income or assets distributed to the individual later. The trust can be fixed or as flexible as you like with discretion given to the nominated trustee over what and when is distributed.

A lineal descent trust is designed to keep your inheritance for your lineal descendants and out of the reach of the Family Court.

Person A dies and leaves their child $700,000 in inheritance.

No trust

Lineal descent trust

It is important that the LDT has been properly drafted otherwise the Family Court may find that its assets are available for distribution.

In the case of families with young children a testamentary trust can help generate extra income to support the surviving family and minimise tax.

This can also provide additional protection if the surviving partner remarries and that marriage subsequently breaks down.

Person A dies and leaves their wife and children $700,000 and 25% shares in husband’s business.

No trust

Testamentary trust

If your children are in high risk professions and have put in place asset protection strategies receiving a direct inheritance can present unanticipated problems.

Person A dies and leaves child $700,000 property

No trust

Testamentary Trust

There are additional costs associated with establishing a testamentary trust and management of the trust upon the death of the testator. These are minimal however in comparison to the benefits the trust provides, particularly in the case where there is significant wealth involved.

Family members can still contest your will so if the distribution of assets amongst the family is not equal it can still be altered.

Every circumstance is different and there is no one-size fits all solution to estate planning. It is important that you discuss estate planning with your accountant and lawyer to come up with the best option for your family. If you haven’t reviewed your estate planning recently, or if you are interested in knowing more about testamentary trusts, please speak to your MGI advisor.

As we approach the end of financial year SMSF holders should use this time for some important housekeeping. Below are 13 things you need to do to maximise the benefits of having a self managed super fund.

SMSFs are required to undertake annual valuations of all their assets for their financial statements and annual audit. See the ATO publication ‘Valuation guidelines for SMSFs’ for more detail.

If you have made considerable gains this financial year it might be worth taking some losses to offset the gains to minimise tax on capital gains (10% for super funds).

Your concessional contribution limit, if you’re under the age of 50 during the financial year, is $30,000 or $35,000 if you are 50 years or older. The non-concessional (after tax) contribution limit is $180,000. If you are under 65 you can bring forward up to two years’ worth of non-concessional contributions, which means you can make $540,000 in one year. Make sure your contributions are received on or before June 30.

Ensure that your Superannuation Guarantee contributions for the June 2015 quarter have been received and that you have accounted for these in your concessional contribution gap.

Salary sacrifice contributions are treated as concessional contributions. Make sure any salary sacrifice contributions have been received by your employer as per your salary sacrifice agreement before contributing additional concessional contributions.

If your partner hasn’t reached their preservation age or is under 65 and has not retired from the workforce you can choose to split up to 85% of your concessional contributions between you and your spouse. You cannot split non-concessional contributions. Splits must be made in the financial year immediately after the one in which your contribution was made. So you can split contributions made in the 2013/14 financial year in the 2014/15 tax return.

If you are under 65 at any time during the 2014/15 year you can access the ‘bring it forward’ rule. So if you have just turned 65 in FY 2014/15 this is your last chance to contribute three times your non-concessional cap in one year.

If so you may be eligible for a full or partial tax offset for spouse contributions up to $3000. The maximum offset available is 18% ($3000 x 18% =$540) but decreases if your partner’s income exceeds $10,800.

If you have a low-income spouse or partner who is engaged in employment, or an adult child who is working part time, you are most likely eligible to access the government co-contribution.

The maximum co-contribution is $500, which is paid when a taxpayer earns less than $34,488 and makes a personal super contribution of $1000. If the tax payer earns between $34,488 and $49,488 the maximum co-contribution is reduced by 3.333 cents for every $1 in excess.

Other conditions to access the co-contribution include that at least 10% of the tax payer’s income must come from employment related activities or carrying on a business (i.e. self-employed), the taxpayer must be under 71 years of age at the end of the financial year and that the person making the super contribution has not claimed it as an income tax deduction.

If you are taking an account-based pension (including a transition to retirement pension) you need to ensure that your SMSF has paid the minimum pension amount by June 30 in order to receive the tax exemption. If you are accessing a pension under a ‘Transition to Retirement” income stream also make sure you do not exceed the maximum limit.

Your SMSF financial statements and audit need to be complete to lodge your tax return. Make sure that you get your records and information ready to send to your accountant. At MGI we will provide you with a list of what information is required by what date.

An SMSF is able to claim tax deductions for a number of expenses including:

While it’s tempting to leave sorting out your SMSF until the last minute it’s best to get started early to make sure that any contributions are received well before the deadline for this tax year (otherwise you risk having the contributions treated as received in the following tax year). Contributions are only recognised when they are received by the superannuation fund’s bank account so make sure you allow plenty of time.

If you have any questions getting your SMSF ready for June 30 speak to your MGI tax adviser today on 3002 4800.

MGI refers to one or more of the independent member firms of the MGI international alliance of independent auditing, accounting and consulting firms. Each MGI firm in Australasia is a separate legal entity and has no liability for another Australasian or international member’s acts or omissions. MGI is a brand name for the MGI Australasian network and for each of the MGI member firms worldwide. Liability limited by a scheme approved under Professional Standards Legislation.

Over 60% of Australians are dying without a will. That number includes people who have incorrect wills and those who don’t have a will at all. How can this be the case in a supposedly highly educated and intelligent country like Australia?

It begs the question – is the traditional Aussie culture of “she’ll be right mate” getting in the way of practical common sense and will it mean that our families will be short changed?

There are a lot of common myths out there in relation to estate planning. And if we don’t know what we don’t know, how can we fix the problem?

Here are seven myths busted to help small business owners get a better understanding so they can better plan their estate, manage their wealth and protect their family by ensuring their assets end up with the people they intended.

This myth is founded on the premise that you “own” all of your assets. This could, in reality, be a fallacy.

For most people, including small business owners, their large value assets include their home and super, which may include life insurance. Whether your family home forms part of your estate will depend on how you hold (or own) the property. Most couples would own their home “as joint tenants”. This means in the event of the death of one of the parties (i.e. tenants), the property automatically reverts to the surviving party (tenant). Your share of the property does not form part of your estate.

Some people (generally unrelated owners of properties) will hold the property as “tenants in common” in agreed-upon proportions (e.g. equal shares). In this case, the death of one “tenant in common” will mean their share of the property will be dealt with in terms of their will and will not go to the survivor co-owner.

It is absolutely crucial you understand how your property is held and therefore whether or not your share of the property will form part of your estate (and dealt with in terms of your will) or not.

The reality is your super is held in a trust, being the super fund, so you don’t actually “own” it. You are therefore reliant on the trustee of your super fund to distribute your super, including any life insurance you have in your super fund, to those you intended it to be distributed to.

Your perception that you “own” your super is entirely that – a perception – unless you have specifically instructed your super fund trustee to distribute it in a certain way. However, you can’t just instruct your super fund trustee in any old way. You have to give them a binding death benefit nomination, or more specifically, a non-lapsing, binding death benefit nomination.

As the description suggests, this nomination is in writing, it doesn’t lapse and therefore remains in place until you revoke it, it is binding on the parties and it nominates who you want your death benefits to go to.

Importantly, every super fund trust deed is different and may contain specific provisions about the form and content of the nomination. It is critical that you specifically follow the requirements of your trust deed to ensure your nomination is binding on the trustee. This is particularly the case where you don’t have a self-managed super fund. In this case, you are reliant on a trustee who you don’t know and have never met, to distribute your super in the manner you had intended. Blind trust – perhaps.

Wrong!

If you die without a will, your state government decides how your estate will be distributed. There are particular rules regarding intestacy (dying without a will). Specifically, the government has a predetermined methodology of determining how to distribute your assets if you die without a will. This may, or may not be, how you had intended them to be distributed.

To illustrate how things can go very wrong, I want to give you a real life example. Recently, a young lady tragically passed away in an accident. She was over 18 years of age and died without a will. As she had no dependents, the intestacy laws in her state prescribed that her substantial death benefit (i.e. life insurance) in her super fund was to be paid equally to her mother and father. Sounds fair enough doesn’t it? The only problem was that the young woman and her mother had been estranged from her father since she was a young child and they had nothing to do with him since then.

Unfortunately, the rules of intestacy meant he ended up with half of her death benefit. Sad, but true.

In most cases, this may well be the case. But what if you are recently divorced from an ex-spouse with children? What if you are in a de facto relationship with someone other than your spouse? What if you are leaving your estate to some children and not to others? What if you are in a “blended” relationship with current and recent ex-spouses, children from prior relationships, step-children? And the list goes on. Do you really want all of your wealth forming part of your estate where it can potentially be challenged?

To the lay person it may seem logical and almost automatic that your assets must form part of your estate. However, for the reasons previously mentioned, there may be valid reasons why you want your estate to contain little, if any, assets. For example, if your will is likely to be challenged.

As discussed, it is possible, in fact probable, that your jointly owned home together with your superannuation will not form part of your estate and therefore beyond challenge. The same goes for interests you may own in a business or other structure, particularly in a trust.

As illustrated by the example in myth 3, even relatively young people can have a sizeable estate due to life insurance held in their super fund. Anyone without a valid will needs to think long and hard about where they want their wealth to end up and where it might end up if they die without a will.

Yes, but . . .

Generally the courts will look at whether the deceased has made “adequate provision” for potential beneficiaries. This might include situations where the deceased leaves a disproportionate share of their wealth to certain children in preference to other children. This could potentially also apply to step children and illegitimate children.

In determining whether adequate provision has been made to a particular party, the courts will look to things such as the size of the estate, the nature of the relationship of the parties, how the estate has been distributed and a number of other factors.

The bottom line is unless “adequate provision” has been made for the respective parties, there is the risk the courts will overrule the will of the deceased and distribute the assets in a different proportion. This shows why, with adequate planning (as discussed in myth 4 above) it may be possible to minimise the size of an estate.

Maybe, and maybe not.

This will depend on a number of factors including the age at which you or your spouse die, the age and marital position of your children and a raft of other issues.

The reality is, fortunately, we’re all living longer. This means if you or your spouse dies relatively young (and to some 60 could be relatively young) there is a fair chance your spouse may remarry or enter into a de-facto relationship. If you leave all your wealth to your spouse (at the expense of your children) there is the possibility they may subsequently break-up with their new partner or spouse and that part of your estate will end up in the hands of their estranged spouse. This won’t make your children happy.

Similarly, even if you spouse doesn’t remarry they may leave the balance of your combined estate to your children. What happens if your children subsequently divorce? Deja vu.

For these reasons, many people’s wills contain a testamentary discretionary trust. In other words, a trust is created on your death and all or part of your wealth is settled on this trust. The beneficiaries of this trust are your blood relatives. Whilst these are not always effective in the Family Court if your spouse and/or children end up there, they probably represent the best protection going around.

A myth is just a widely held, but mistaken, belief. Don’t be hoodwinked by estate planning myths. Everyone’s situation is different, so also don’t do something just because friends have done it. Get professional advice about your specific situation. The cost of doing things right now will pale into insignificance compared to the cost to your estate (and your loved ones) in getting it wrong, particularly dying without a will.

MGI South Queensland offers a range of estate planning and wealth management services including asset protection strategies to preserve wealth within families. Talk to your MGI Gold Coast or Brisbane Accountants today and make sure your assets end up with the people you intend. Call 3002 4800.