Subscribe for Our Latest Resources

"*" indicates required fields

This morning the Queensland Government introduced a $260 million grant for small to medium businesses who have been affected by the two recent lockdowns.

Eligible businesses will receive $5,000 (excluding GST) to use for any business expenses and to support cash flow through the Covid Lockdown. Your business does not have to be located in South East Queensland to be eligible for the grant.

To be eligible for the grant, your business must have experienced a reduction in turnover of at least 30% as a result of the lockdown.

Small & Medium Businesses are defined as having:

You will need to apply online with supporting evidence. The funds will be paid into your bank account within 2 weeks of the application being processed and approved.

More specific information about the grant including opening date will be available within the coming days.

If you need assistance regarding your grant application, please do not hesitate to contact our Team.

The alternative decline in turnover test for JobKeeper fortnights from 28 September onwards has been released by the ATO.

The new alternative tests are in line with the original covering the 7 circumstances outside the usual business operation that resulted in your 2019 relevant comparison period not being appropriate for applying the basic decline in turnover test.

This includes the following:

Below are some of the key changes that you should take into consideration when applying the appropriate tests

As with the previous alternative test or the basic decline in turnover tests, you will need to maintain sufficient and appropriate documentation on how the tests have been applied in case of an ATO review.

Please feel free to contact the team at MGI South Queensland if you wish you to discuss the application of the alternative test to your circumstances.

The Government has announced the extension of the JobKeeper Payment until 28 March 2021 and is targeting support to those businesses that continue to be significantly impacted by the Coronavirus.

From 28 September 2020, eligibility for the JobKeeper Payment will be based on actual turnover in the relevant periods and the payment will be stepped down and paid at two rates.

To be eligible for JobKeeper Payments under the extension, businesses and not-for-profits will still need to demonstrate that they have experienced a decline in turnover of:

In order to be eligible for the JobKeeper Payment from 28 September 2020, businesses will have to meet a further decline in turnover test for each of the two periods of extension, as well as meeting the other existing eligibility requirements for the JobKeeper Payment.

To be eligible for Jobkeeper payment from 28 September 2020 to 3 January 2021

Businesses will need to demonstrate that their actual GST turnover has fallen in the September quarter 2020 (July, August, September) relative to a comparable period (generally the corresponding quarter in 2019).

To be eligible for the second JobKeeper Payment extension period of 4 January 2021 to 28 March 2021

Businesses and not-for-profits will need to demonstrate that their actual GST turnover has fallen in the December quarter 2020 (October, November, December) relative to a comparable period (generally the corresponding quarters in 2019)

The Commissioner of Taxation will have the discretion to set out alternative tests that would establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019

From 28 September 2020 to 3 January 2021, the JobKeeper Payment rates will be:

From 4 January 2021 to 28 March 2021, the JobKeeper Payment rates will be:

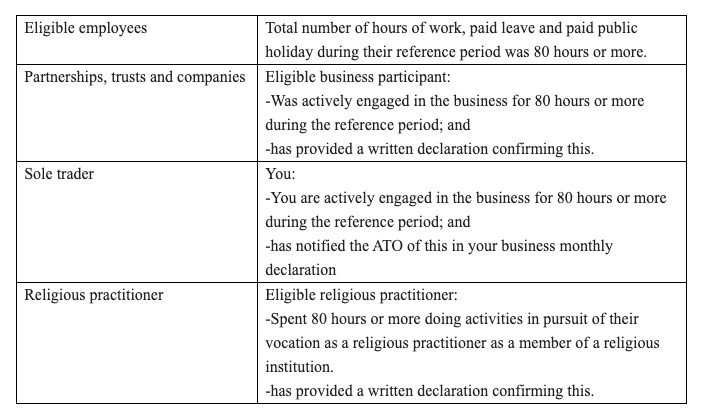

Employees are eligible in the extension period if they:

Were either:

Only one employer can claim the JobKeeper Payment in respect of an employee

The self-employed will be eligible to receive the JobKeeper Payment where they meet the relevant turnover test, and are not a permanent employee of another employer. Employees will continue to receive the JobKeeper Payment through their employer during the period of the extension if they and their employer are eligible and their employer is claiming the JobKeeper Payment. However, the amount of the JobKeeper Payment will change at the rates set out above.

Please contact our office if you wish to discuss your personal circumstances and how to meet the eligibility criteria.

The government has announced that the current $1,500 per fortnight JobKeeper payment will continue past 27 September. However, it will be reduced to $1,200 per fortnight from 28 September, and $750 per fortnight for employees working less than 20 hours a week.

From 4 January, the rate will fall to $1,000 per fortnight and $650 for people working less than 20 hours a week.

Full details of the updated JobKeeper program can be found here.

Businesses looking to remain on JobKeeper beyond 27 September will be required to meet new eligibility tests.

Businesses will still be required to demonstrate the required reduction in turnover i.e. 30 per cent for businesses with turnovers of $1 billion or less, 50 per cent for those with turnover of more than $1 billion, and 15 per cent for ACNC-registered charities.

The current JobKeeper programs requires a business to apply the test for one period (a month or a quarter) prospectively. However, the government will now require businesses to reapply the tests for the June and September quarters to be eligible for JobKeeper beyond September.

In addition, businesses will need to demonstrate that they have met the relevant decline in each of the three quarters ending on 31 December 2020 (June, September and December quarters) to remain eligible for the payment from January 2021 to March 2021.

We will continue to update this post once more details are known.

Please contact your MGI South Queensland advisor should you have any queries.