Subscribe for Our Latest Resources

"*" indicates required fields

We have put together a summary from our recent Webinar covering Inter-Generational Wealth Transfer and Estate Planning with the help of our presenters Zee Zhang – Director at MGI, Jaxon King – Managing Director at Scion Private Wealth and Michael Klatt – Partner at Mullins Lawyers.

Presented by Zee Zhang

Estate planning isn’t just paperwork – it’s a powerful way to ensure that your hard-earned wealth smoothly transfers to those you love, without unnecessary stress or tax bills. In our recent webinar, “Family Wealth Transfer & Navigating Estate Planning Issues,” we unpacked a simple yet powerful way to approach your wealth: the Four Buckets Framework.

Families often underestimate how critical early planning is until it’s too late. Here are three big reasons why acting sooner rather than later is essential:

We introduced attendees to our easy-to-follow “Four Buckets” model:

Beyond buckets, successful family wealth transfers also rely on good governance. We recommend four foundational tools:

Effective estate planning involves collaboration between:

Start with these practical steps today:

Estate planning is not just about the money – it’s about preserving family harmony and ensuring your legacy goes exactly where you intend. Act early, and you won’t just be planning your estate; you’ll be safeguarding your family’s future.

For any questions about this topic, please contact Zee Zhang on (07) 3002 4800 or email zzhang@mgisq.com.au.

Book your complimentary 1-hour structuring review today with Zee and gain clarity on your family’s financial future.

Presented by Jaxon King

As the landscape of superannuation and tax legislation evolves, so too must our strategies for protecting and transferring wealth. With the introduction of Division 296 into Australian tax law, many high-net-worth individuals are now facing a new challenge: how to manage the growing tax burden on their superannuation balances – particularly when planning for future generations.

This article will explore the implications of Division 296, outline key strategies to mitigate its impact – such as investment bonds and superannuation recontribution strategies – and provide guidance on how to turn complexity into opportunity for your family legacy.

Division 296, part of the Treasury Laws Amendment (Better Targeted Superannuation Concessions) Act 2023, introduces an additional 15% tax on earnings attributable to superannuation balances exceeding $3 million, effective from 1 July 2025.

This tax is applied to “earnings” on the portion of your total super balance that exceeds $3 million, regardless of whether the earnings are realised or unrealised.

Key Points:

High-income professionals, business owners, and self-funded retirees who have built significant retirement savings are the most exposed. While the legislation targets a relatively small cohort now, indexation is not applied to the $3 million cap, meaning more Australians will fall under its scope in time.

Even without Division 296, many Australians with large superannuation balances face another tax trap: the taxable component of their super may be subject to up to 17% tax when passed to non-dependent beneficiaries (e.g. adult children)

Why It Matters:

So, how do we manage these risks while preserving your legacy?

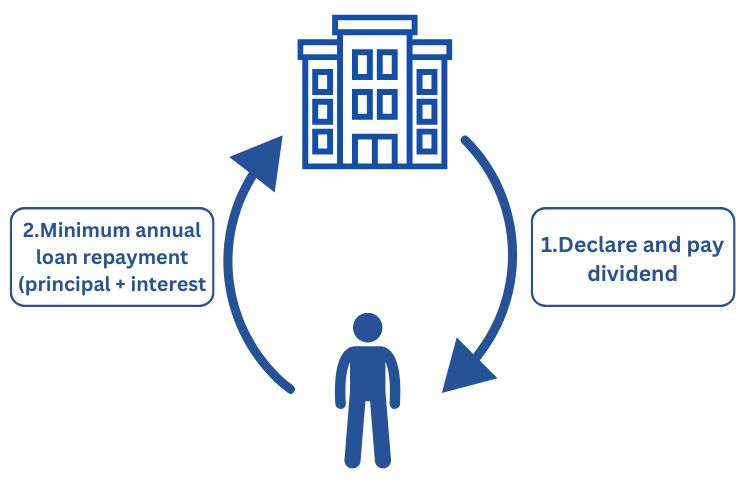

A recontribution strategy involves withdrawing money from your superannuation and recontributing it back as a non-concessional contribution. This effectively converts the taxable component into tax-free, reducing the potential death benefits tax payable by non-dependent beneficiaries.

Benefits:

How It Works:

Contribution Limits to Watch:

Non-concessional cap: $120,000 per year, or $360,000 over 3 years under the bring-forward rule.

Must be under age 75 and meet the total super balance test (less than $1.9 million to make non-concessional contributions).

Investment bonds are a powerful, often overlooked, tool for building and transferring wealth outside the superannuation system – making them an excellent complement to Division 296 planning.

Key Features:

Ideal Uses:

Strategic Benefits:

While tax and investment strategies are crucial, the real risk to generational wealth is not legislative—it’s relational.

More than 70% of wealth transfers fail by the second generation, not because of poor tax planning, but due to lack of communication and family alignment.

Start with These Steps:

The Cost of Doing Nothing

You’ve spent decades building your wealth. The final, and perhaps most important step, is ensuring it serves your family – not just financially, but relationally – for generations to come.

Every family is unique, and so is every wealth transfer plan.

For any questions about this topic, please contact Jaxon King on 07 3778 6800 or email JKing@scionprivatewealth.com.au

You can also book a Complimentary Strategy Session with Jaxon

He is currently offering a limited number of 30-minute one-on-one calls to:

Presented by Michael Klatt

Approximately 50% of the Australian population does not have a valid Will. This seems to be a result of complacency, largely, but also, in some circumstances, testators find it difficult to decide on how to distribute their estate following their death. This is particularly the case where the testator is a member of a blended family.

Estate planning is more than just making a Will. It is also important to have an Enduring Power of Attorney by which a person can authorise an attorney to act in relation to their financial affairs and personal (including health) matters. This document terminates on the person’s death.

It is important to identify how assets are owned. Sometimes, assets are owned by an individual; other times, they are owned jointly with one or more other persons. Assets can also be owned by a company or trustee of a trust, including family trusts or units trusts. Assets can also be held by a superannuation fund, either a self-managed superannuation fund controlled by the members or a retail or industry fund controlled by the trustees of those retail or industry funds. It is not uncommon for clients to not fully appreciate where the assets sit.

Once assets and liabilities are identified, it is necessary to consider the personal circumstances of the testator; are they married or in a relationship, do they have children, are they in a blended family situation, are there any issues of estrangement with family members that need to be considered, do family members who are identified as potential beneficiaries get on?

It is necessary to consider who to appoint as an executor or executors of the Will. These should be responsible people, not merely people who would expect to be appointed as executors. Appointing the right people to act as executors is crucial in avoiding family disputes.

If multiple executors are being appointed, then they need to be able to work together. Sometimes, it is appropriate to appoint an independent executor, either a friend or a professional advisor, particularly where the testator may be in a blended family situation. In the event that executors are not able to work together, the likely scenario will be a beneficiary or executor making an application to the court for the removal of the executors and the appointment of an independent administrator, typically an independent lawyer.

Typically, if children are not treated equally in the division of a testator’s estate, a family dispute will arise. Sometimes, however, a testator may feel that one child should receive a larger portion of the estate and other children, particularly where the testator may have a family business and one child has contributed significantly in the improvement of the family business to that child’s detriment, particularly also where they have not been paid a commercial rate of salary for the effort provided. Careful planning is necessary when developing an estate plan in these circumstances. If it is possible to distribute non-family business assets to children not involved in the business, then that is typically the preferred course of action.

Communication with family members in relation to the testator’s estate plan is usually advisable. This may prevent family disputes after a testator’s death, but this is not always the case.

The advice to testators who are members of a blended family is generally that, if it is possible to leave an inheritance to the testator’s children of a previous relationship in circumstances where their new spouse is still living, then this assists with potentially avoiding a family dispute after the testator’s death. Again, this is not always the case. Sometimes, there are insufficient assets to provide for adult children of a previous relationship and the new spouse. Testators may well consider entering into a mutual Will deed with their spouse by which they promise to leave their estate a certain way in the event that their spouse pre-deceases them.

Generally, children co-owning assets that have been left to them by their parents does not work. Careful consideration needs to be had before a decision to leave assets to children to be co-owned is made. If, however, it is decided that children will co-own assets, particularly in the situation of a family business, then proper governance needs to be put in place. Family Charters, Family Constitutions, Shareholders Agreements, and Unitholders Agreements are all tools that can be used to assist with avoiding a family dispute in a co-ownership arrangement.

Some testators have control of a family trust. A family trust is typically a discretionary trust where no one beneficiary has an absolute entitlement to the assets held by the trustee of the trust. Careful consideration needs to be given to the succession of control of the trust and, to the extent that the testator is able, they should leave wishes as to how the trust assets should be administered.

Clients with any significant wealth are typically concerned about leaving an inheritance to their children and their children subsequently separating from their spouse, exposing the inherited assets to a family court property settlement. Accordingly, many testators decide to incorporate testamentary discretionary trusts in their Will. Instead of leaving the inheritance directly to the child, the inheritance is left to the child as trustee for a testamentary discretionary trust. The beneficiaries of that trust include the child as the primary beneficiary and then other discretionary beneficiaries, including the child’s children and other relatives. Sometimes, spouses of the child and other beneficiaries are included as beneficiaries but are limited to being income beneficiaries and not capital beneficiaries. Proper consideration of the terms of those testamentary discretionary trusts is important. There is no standard testamentary discretionary trust Will that will suit all testators.

It is important that clients have Enduring Powers of Attorney in place. These documents are not just for elderly clients. One never knows when they may have an accident and therefore not be able to manage their own finances and personal health matters. Again, proper consideration as to who to appoint as attorneys is imperative. These are not documents that can simply be printed off and completed by clients without professional guidance.

It is vital that clients surround themselves with competent advisers, including a lawyer, an accountant, and a financial planner and that all of these advisors are engaged to assist with the estate planning exercise.

For any questions about Wills and Estates, please contact Michael Klatt on (07) 3224 0370 or email mklatt@mullinslawyers.com.au

We have put together a summary from our recent Webinar covering PCG2021/4 and Wealth Structuring for Paediatric Dentists with the help of our presenters Alice Wu – Associate Director of MGI and Jaxon King – Managing Director of Scion Private Wealth.

PCG 2021/4 is a Practical Compliance Guideline issued by the Australian Taxation Office (ATO). It outlines how the ATO assesses the allocation of profits within professional firms, especially where income is distributed through structures like trusts, partnerships, or companies. It applies to individual professional practitioners (IPPs)—such as directors, partners, or shareholders—who derive income from professional services firms.

This guideline is relevant for:

The ATO has confirmed that PCG 2021/4 remains in effect for the 2025–2026 financial year. Staying within the green zone (low risk) is essential because it:

Before scoring your arrangement, you must pass two gateways:

Then, assess your arrangement using up to three risk factors:

Vinnie runs his dental practice through a company owned by the Wen Family Trust. He’s entitled to $400,000 in total income.

This setup scores 8, placing Vinnie in the amber zone (medium risk). Because his market salary is hard to benchmark, only two risk factors are assessed.

However, if Vinnie adjusts the distribution so that 60% of the income stays in his name, his score drops to 7, moving him into the green zone—a much safer position.

For any questions about this topic, please contact Alice Wu on (07) 3002 4800 or email awu@mgisq.com.au

How specialist dental professionals can structure their wealth and invest strategically to turn today’s business income into tomorrow’s financial freedom.

Running a successful dental practice – particularly in specialist areas like paediatric dentistry – comes with more than just high income. You face unique challenges: complex income structures, specialist equipment costs, staff obligations and potential litigation risks.

While compliance with PCG 2021/4 is essential for meeting tax obligations, it’s what you do with that income afterward that defines your long-term financial success. In this article, we explore the strategies discussed in our recent AAPD webinar, turning expert insights into practical advice to help you turn tax-smart profits into lasting personal wealth.

At Scion Private Wealth, we use a proven framework to guide our high-income clients:

1. Structure – Protect, Distribute & Grow

2. Strategy – Make Money Work Harder Than You Do

3. Succession – Plan Ahead for Life Beyond the Practice

Dentists need asset protection and tax efficiency. Here’s how different structures compare:

Best Practice: Use a combination – e.g., a company to operate the practice, a service trust for income splitting and a family trust to distribute profits tax-effectively.

The ATO’s guidelines around income allocation don’t eliminate trusts- they just raise the bar for consistency and evidence.

To stay in the green zone:

Case in Point: Dr Sarah, a paediatric dentist, restructured her trust for compliance while using excess profits to fund a family investment company for her children’s future.

Dentistry is a high-liability profession. Lawsuits, staff disputes, or even property leases can place personal wealth at risk.

Asset Protection Strategies:

When structured well, surplus profits can fund assets that pay you – even while you sleep.

Options to Consider:

Dr James invested $100K annually into global healthcare and infrastructure funds. Five years later, his portfolio now generates $32,000 in passive income annually.

Super can be a secret weapon for dentists- especially as high-income earners facing top marginal tax rates.

Key Tips:

Your personal wealth journey can also support the next generation.

Tax-Efficient Options for building intergenerational wealth:

Many dentists delay practice succession planning until it’s too late—or worse, sell without a strategy.

Exit Pathways:

Dr Helen gradually transitioned her practice to a junior dentist, retained the clinic’s building, and now earns $60K per year in rental income while mentoring part-time.

Your practice should support your life – not the other way around.

Use surplus income to:

“You’ve built a great practice. Now it’s time to build a great life.”

Too many high-income professionals leave wealth to chance. A strategic, tailored approach can mean the difference between a busy working life and a truly wealthy one.

Key Takeaways:

Let’s explore how your business success can fund your long-term lifestyle goals.

For any questions about this topic, please contact Jaxon King on (07) 3778 6800 or email jking@scionprivatewealth.com.au.

Scion Private Wealth is a trusted advisor of MGI.

The Australian Taxation Office (ATO) has shared the specific risks it will be monitoring for the 2024-2025 tax year. Following on from the small business focus areas identified in Quarter 4 of the this year and on the warnings it issued for the last financial year, there are a number of issues that remain firmly at the top of the list when it comes to tax compliance. As the 2025 end of tax year approaches, the ATO is sharpening its focus on several key areas to ensure compliance and integrity within the tax system. This year, the ATO is particularly vigilant about claims for rental property deductions, work-related expenses, cryptocurrency and undeclared income from the sharing economy. If you’re preparing for tax time, understanding and ensuring you’re fully compliant in these areas can help ensure you get your lodgment right the first time. Let’s take a look at the ATO focus areas for tax time 2025 in a bit more detail.

Investment properties were a firm focus at tax time in 2024 and the ATO continues to scrutinise rental property deductions closely, ensuring that claims are legitimate and accurately reflect expenses incurred. Recent audits from the tax office indicate that 90% of rental property owners are getting their tax returns wrong.

According to ATO Assistant Commissioner, Robert Thomson: “People aren’t apportioning correctly between interest relating to private use and the interest that relates to the income they’re generating from their investment property.”

Common areas where taxpayers might encounter issues include:

The ATO employs sophisticated data-matching techniques and collaborations with financial institutions to identify discrepancies and ensure compliance. Rental property owners should maintain detailed records and seek professional advice to ensure their claims are accurate and justifiable. A registered tax agent can help ensure your tax return is accurate.

As in the previous couple of years, work-related expenses are another area under the ATO’s microscope. Changes were made in 2023 to the fixed rate method of calculating a working from home deduction and taxpayers were required to keep more detailed documentation. However, as these rues have now been in place for a couple of years the expectation is that you must have comprehensive records to substantiate your claims.

“Copying and pasting your working from home claim from last year may be tempting, but this will likely mean we will be contacting you for a ‘please explain’. Your deductions will be disallowed if you’re not eligible or you don’t keep the right records.” Mr Thomson said.

To avoid issues, taxpayers should adhere to the following guidelines:

Accurate record-keeping and adherence to ATO guidelines are essential to ensure compliance and avoid audits or penalties.

Remember, there are 3 golden rules for claiming a deduction for any work-related expense:

The rise of the sharing economy has introduced new challenges for tax compliance. Platforms like Airbnb, Uber, and various freelancing sites have made it easier for individuals to earn income that may go undeclared.

The ATO is particularly focused on:

The ATO collaborates with sharing economy platforms to access data and identify undeclared income. These sophisticated data matching systems mean that if you decide to not report your income from these platforms then you are much more likely to trigger a review by the ATO. Participants in the sharing economy should maintain comprehensive records of their earnings and report them accurately to avoid penalties.

Cryptocurrency and crypto based business models are an emerging area of focus for the ATO. Australian tax payers have been warned that they need to report all cryptocurrency related capital gains, losses and income in their tax returns. The Australian Taxation Office treats cryptocurrency as property for tax purposes. This means that individuals and businesses are required to pay capital gains tax (CGT) on cryptocurrency transactions, depending on the profits they make.

When you sell a cryptocurrency asset you need to work out whether you made a capital gain (i.e. you made a profit) or a capital loss (i.e. you lost money) to determine how much capital gains tax (CGT) you’re required to pay. You need to report your gains and losses in your tax return and pay income tax on net gains.

It’s also important to understand whether you’d be considered an investor or a trader for tax purposes. If you buy and sell assets regularly, you may be considered a trader, which changes the taxation treatment of any gains or profits you make on your asset sales.

The advice is also to not rush to submit your tax return, particularly if you received income from multiple sources. “By lodging in early July, you are doubling your chances of having your tax return flagged as incorrect by the ATO.”

As the ATO intensifies its focus on rental property deductions, work-related expenses, cryptocurrency and undeclared income from the sharing economy, it is more important than ever for taxpayers to be diligent and compliant. By understanding the ATO focus areas and maintaining accurate records, taxpayers can navigate their obligations confidently and avoid the risk of audits and penalties. If in doubt, seeking professional advice from the tax experts at MGI can provide the necessary guidance to ensure compliance and peace of mind in the 2025 tax year.

Check out our recent blog on Personal Services Income (PSI) to ensure that you are categorising your business and services correctly.

For more information or personalised advice on your tax obligations, feel free to reach out to the experts at MGI South Qld. We’re here to help you navigate the complexities of the Australian tax system with ease and confidence.

You might also be interested in our most recent blog on the ATO small business focus areas for Q4 of the 2024/25 financial year.

The Australian Taxation Office (ATO) has recently released an updated set of small business benchmarks based on 2022-23 financial year data. The benchmarks are reviewed annually and broken down into 100 industries and they’re used by the ATO to assess whether a business might be under-reporting taxable income and over-claiming deductions.

The ATO provides Small Business Benchmarks as a tool to help businesses compare their financial performance against industry standards. These benchmarks are derived from data collected from tax returns and activity statements of businesses across various industries. They serve as a guide for businesses to assess their performance and ensure they are meeting their tax obligations.

The ATO uses these benchmarks to identify businesses that may be avoiding their tax obligations. By comparing a business’s financial ratios to industry standards, the ATO can detect anomalies that may indicate underreporting of income or overstatement of expenses. Businesses that fall significantly outside the benchmark ranges may attract scrutiny and potential audits.

However, they can also be a useful tool for any business to compare your performance, including turnover and expenses against others in your industry. You might be able to identify opportunities to make improvements to your business.

The benchmarks cover 100 industries and over 2 million small businesses around the country. The industries include:

What If Your Business Falls Outside the Industry Benchmarks?

You might find that your business falls outside of these benchmarks. If you’re above or below the standards for your industry it doesn’t necessarily mean you’ve done anything wrong however, it’s an indicator that it’s worth reviewing your business plan.

ATO Assistant Commissioner Tony Goding said: “While we never use the benchmarks in isolation, small businesses who fall outside the ATO’s benchmarks are more likely to trigger a closer examination from us to identify if they are making mistakes or deliberately doing the wrong thing.”

If your business’s expenses are higher than the industry average, it may suggest that your expenses are high relative to sales. This might show that your:

Such discrepancies can trigger ATO reviews or audits to ensure compliance.

Conversely, if your expenses are significantly lower than the industry average, it might indicate that:

While being below the benchmark isn’t inherently negative, it’s essential to ensure that all expenses and obligations are accurately reported.

Understanding where your business stands in relation to the ATO Small Business Benchmarks is crucial. Regularly comparing your financial ratios to industry standards can help identify areas for improvement and ensure compliance with tax obligations. It also aids in making informed business decisions and maintaining financial health.

At MGI South Qld, we specialise in business performance analysis and helping businesses navigate the complexities of tax compliance and financial performance. Our team can assist you in:

Contact us today to ensure your business aligns with industry benchmarks and maintains robust financial health.

Loans now available for disaster-affected businesses from the Western Queensland surface trough and associated rainfall and flooding.

Financial assistance is available for primary producers, small businesses and not-for-profits impacted by flooding in Western Queensland.

Disaster Assistance Loans and Essential Working Capital Loans have been activated for businesses in Barcoo, Boulia, Bulloo, Diamantina, Longreach, Murweh, Paroo, Quilpie, and Winton local government areas.

These loans are designed to support small businesses to re-establish operations relating to:

Eligible primary producers, small businesses and not-for-profits can apply for:

For more information on eligibility and how to apply – follow these links: Disaster Loans and Disaster Assistance (Essential Working Capital) Loans

Should you have any questions or wish to discuss this matter further, please do not hesitate to contact the team at MGI.