Corporate beneficiaries are a popular and effective strategy for delaying tax. However if you use a corporate beneficiary it’s important that you remember just that; it is a delaying strategy.

Recently I have noticed a number of new clients telling me that their previous accountant saved them a fortune through the use of a corporate beneficiary. What is evident in these conversations is that they are not aware of, or have forgotten that this is not the “end story”. If they plan on spending the profits, then they will be required to start paying back some (maybe all) of the tax saved, over a period of time. And in the context of this law, the government makes no concession if you have reinvested the profits back into legitimate business working capital. The danger here is that you might think you are “all done” in terms of tax, and then spend all remainding cash. When it comes time to pay the deferred tax all your funds are gone! What’s worse, you have been deferring the tax on multiple years’ profits, so that you end up with an unmanageable tax debt to pay. It’s a trap that we see happening all the time. With so much confusion around corporate beneficiaries, let’s revisit what a corporate beneficiary is and why you might chose to use them.What is a corporate beneficiary?

The individual tax rate can be as high as 47% including the Medicare levy. This compares to the company tax rate of 30%. If you generate profits through a trust, you might form and use a corporate beneficiary, to distribute profits to, and be taxed at the lower 30% tax rate. Obviously it is better to have 70 cents to reinvest in your business, rather than 53 cents, and therefore it is a strategy many have employed. But, as mentioned before, this is not the end of the story. Usually this arrangement means there is still an unrealised tax debt to be managed over a period of time. (Generally up to seven years).Where issues arise

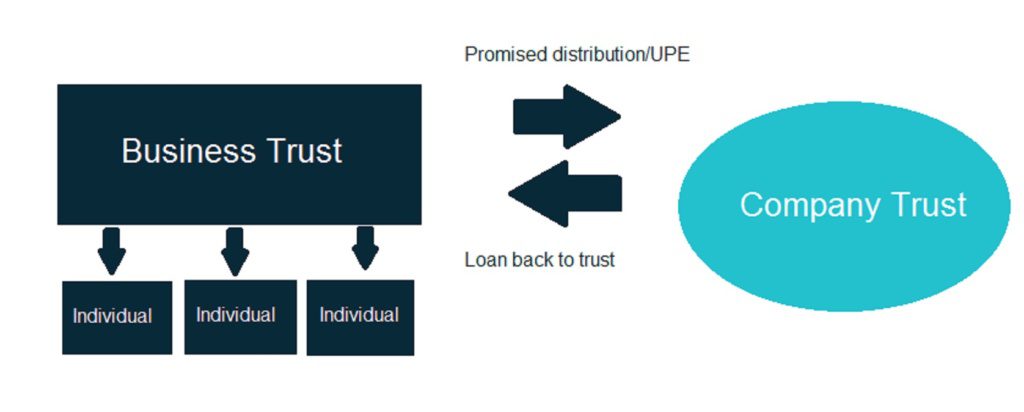

It’s important to understand that the arrangement requires the trust “promising to pay” profits, to that corporate beneficiary. The issues start to arise because often the funds are not actually paid over to the company, (usually because they have already been spent). This means that there are accounting entries and loan documents required to record the declared profits as an “unpaid present entitlement” (UPE) to the company, and also a loan back to the trust.

The law says, if you engage in this arrangement then you must either;

- Transfer real cash to the company to invest, or;

- Enter into a loan agreement from the company to the trust, charge interest, and make yearly minimum repayments calculated by a particular formula defined in the law.

If this does not happen, then the funds must be declared as a dividend and you must pay tax on that immediately. And worst of all, unlike normal franked dividends, it will likely be treated as unfranked dividend, on which tax is paid at your full marginal rate, receiving no benefit for the 30 cents in the dollar already paid at the company level.

In other words, if you don’t follow the law then you must pay back all of the tax saving you thought you had, plus more.

What most do

Our experience is that often businesses do not often have spare cash to transfer over to the corporate beneficiary, nor even to make annual minimum payments.

Or alternatively they simply choose not to pay cash across to the corporate beneficiary (or to pay the tax) because they believe can use the funds to generate a higher return in their business. Why borrow from the bank when you have these funds to invest?

Most end up entering into an unsecured loan agreement over the permitted maximum term of seven years, offsetting the annual required minimum repayments and interest by declaring “on paper” fully franked dividends.

But, the dividends are not paid in real cash. They are an accounting and tax entry only, to serve the purpose of reducing the value of the loan within the required period.

Even though no cash has changed hands, the business owner is then required to pay additional “top up” tax on those dividends, being, the difference between the corporate tax rate of 30% and their marginal rate.

As no cash is actually paid, there is a cash flow timing issue. The “top up” tax must be funded either with future income, selling assets, or drawing on savings if there is any.

In some situations, no top up tax is required to be paid. In fact a tax refund is issued because the year in question, has not been as good as prior years and so the business owners now have access to marginal rate that is lower than 30%. A credit is obtained for the tax already paid at the company level, and a refund is issued.

It’s worth mentioning also that the loan payback period can extend from 7 to 25 years if there is any spare equity in property, over which the loan might be secured. Extending the loan payback period means a much longer time period over which to manage the required dividends, and possibly providing the opportunity to manage the dividends to access lower tax brackets.

But our experience is that most entrepreneurs have their equity fully expended on other projects, and therefore this is not generally a practical option.

How to use a corporate beneficiary to your advantage

The following situations present an opportunity to use a corporate beneficiary to your advantage.

1. If you have an unusual year or couple of years.

A corporate beneficiary provides the benefit of smoothing out the tax over years of lumpy income.

For example, when you sell a property or have an unusually good business year, you might otherwise be pushed into a higher than normal tax bracket.

2. You are near retirement

If you are near retirement, or any other planned break in employment, this might allow you to declare dividends to you over the periods are in a lower tax bracket.

For some this could even mean a refund of tax previously paid by the corporate beneficiary.

3. You have spare cash that you want to quarantine from the risks attached to the business operation and can’t (or don’t want to) put any funds into super.

Superannuation is one of the best investment vehicles there is for lots of reasons, including taxation, asset protection and generally quarantining your savings.

However for many reasons, it’s not always a suitable place to park funds, particularly if you intend on using that money for your business later, wish to highly gear, or you wish to invest in assets, which super law doesn’t allow.

As an alternative, your corporate entity could invest your funds in a much larger range of assets, with higher gearing ratios. Also this would provide another barrier to business risk, and provide the flexibility of being able to access funds for future business ventures.

And if your company is investing in shares that pay fully franked dividends, the tax is already paid before it gets deposited into your company bank account. There is no more tax to pay.

At this point it is appropriate to mention that the 50% general Capital Gains Tax (CGT) discount is not available to a company. Whereas it is to individuals and trusts. But, many high net wealth individuals are happy to forgo this in consideration of the following:

- Declaring distributions to invest outside the company would mean too much tax comes off the top

initially from the investing capital. - The complexity and cost of otherwise accounting for statutory loans as described above

- Financial Institutions, find the alternative use of statutory loan arrangements lack transparency, and

therefore obtaining debt finance is impeded, or more costly. - The additional protection a company structure provides in comparison with investing in personal

names. - In consideration of all the disadvantages, the margin between a company tax rate 30% is not that much

higher than 23.5% (being the effective rate after the 50% general discount is applied to the top

marginal rate of tax of 47% including Medicare) - And anyway, some assets are otherwise eligible to obtain a small business concessions of between 75%

and 100% of the gain made. So the 50% general discount isn’t needed.

4. You know the deal, but where else would you put the funds for better use for the next seven years?

As long as you are not worried about carrying a future tax liability (and keep this in mind in your plans) using a corporate beneficiary can be tax efficient.

BUT, and here is the big but, you need to keep in mind that you are complicating your affairs and eventually you will need to deal with the tax at your personal marginal rates.

If you decide a corporate beneficiary would be advantageous, make sure you discuss this strategy with an experienced accountant and run through what you will need to pay back, and when.

Our experienced tax consultants can advise you further on this.

Restructure from a Trust to a Company?

It’s also worth pointing out that there are legitimate tax concessions which permit the roll over of a business’ tax free from a trust to a company structure. Having the business in a company permits the business to reinvest that 70c in each dollar into working capital without the complications mentioned above of a corporate beneficiary.

The catch of course is that stamp duty concessions are not available in most states (and in particular Queensland).

A cost benefit analysis would be required.